What is the best broker for learning price action?

For most traders in 2026, Deriv offers the strongest combination of charting flexibility, execution quality, and learning opportunities.

Is price action better than indicators?

Price action is not necessarily better. However, many experienced traders use price action as their primary decision-making framework and indicators as supporting tools.

Can beginners learn price action?

Yes. In fact, many traders learn faster when they focus on price behavior before adding multiple indicators.

Why Traders Move from Binomo to Deriv in 2026: The Real Reasons Behind the Switch

If you spend enough time around trading communities, you’ll notice a pattern.

Many traders start with Binomo.

Then, after a few months, a surprising number begin looking at Deriv.

Some switch completely.

Others keep both accounts but gradually move most of their trading activity to Deriv.

I noticed this trend while talking to beginner traders who initially chose Binomo because of its simplicity. The platform is easy to understand, the interface is clean, and placing a trade takes only a few seconds.

But as traders gain experience, their priorities often change.

They stop asking:

“How easy is this platform?”

And start asking:

“How much flexibility does this platform give me?”

That shift is often what starts the journey from Binomo to Deriv.

One of the biggest reasons traders move to Deriv is variety.

Binomo focuses heavily on short-term fixed-time trading.

Deriv offers a much wider ecosystem.

Depending on your region, traders may access:

Forex

Synthetic Indices

Commodities

Multipliers

CFDs

Derived Markets

For traders who eventually feel restricted by a single trading format, this broader selection becomes attractive.

Many traders report that they don’t necessarily leave Binomo because it’s bad.

They leave because they outgrow its limitations.

Traders looking for access to forex, synthetic indices, commodities, and advanced trading products often begin their journey with Deriv.

Reason #2: Synthetic Indices Have Created Huge Interest

Synthetic indices have become one of the hottest topics in online trading.

Unlike traditional markets that depend on economic events or market opening hours, synthetic indices operate continuously through proprietary algorithms.

This appeals to traders who have limited time during market hours, live in different time zones, or want trading opportunities throughout the day.

As interest in synthetic indices continues growing, many former Binomo users naturally migrate toward Deriv.

After talking with hundreds of traders over the years, one pattern appears repeatedly.

Most people do not switch brokers because of a single feature.

They switch because another platform better matches their current stage of development.

A complete beginner values simplicity.

An intermediate trader values flexibility.

An advanced trader values tools, market variety, and strategic freedom.

The move from Binomo to Deriv often reflects that progression.

Thinking About Moving Beyond Binomo?

If you’re ready to explore a wider range of markets, synthetic indices, forex, and advanced trading tools, Deriv is one of the first platforms most experienced traders test.

Before You Switch Brokers

Before changing platforms, ask yourself whether you’re switching because the platform is limiting you, or because you haven’t yet developed a consistent strategy.

A lot of beginners enter trading with the same question:

“Is $10 actually enough to start trading on Deriv?”

The short answer is yes.

But the real answer is more complicated.

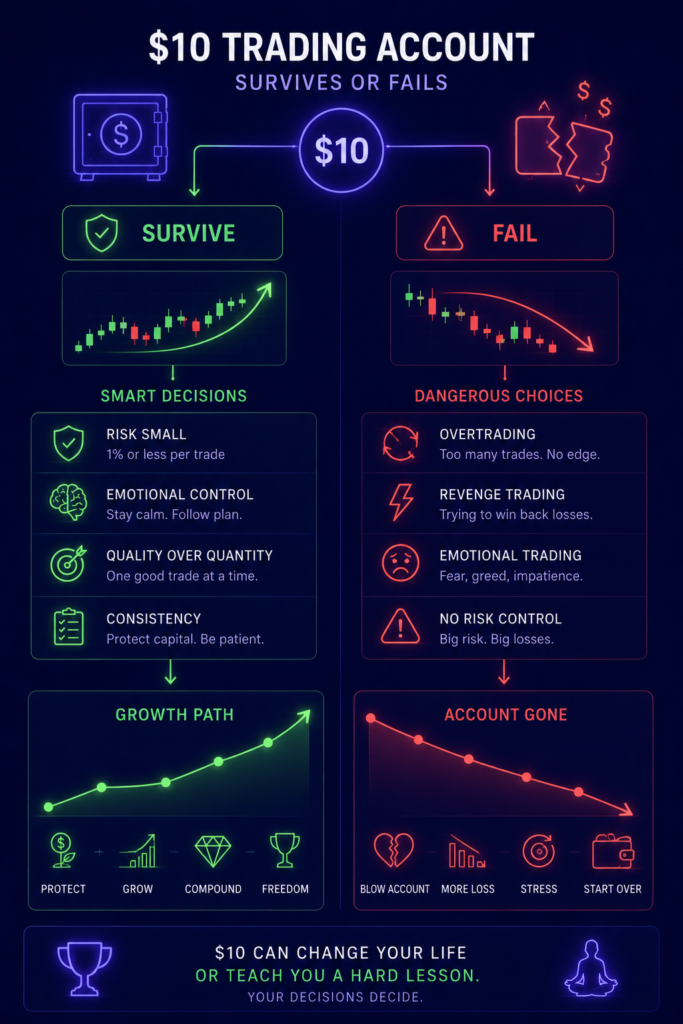

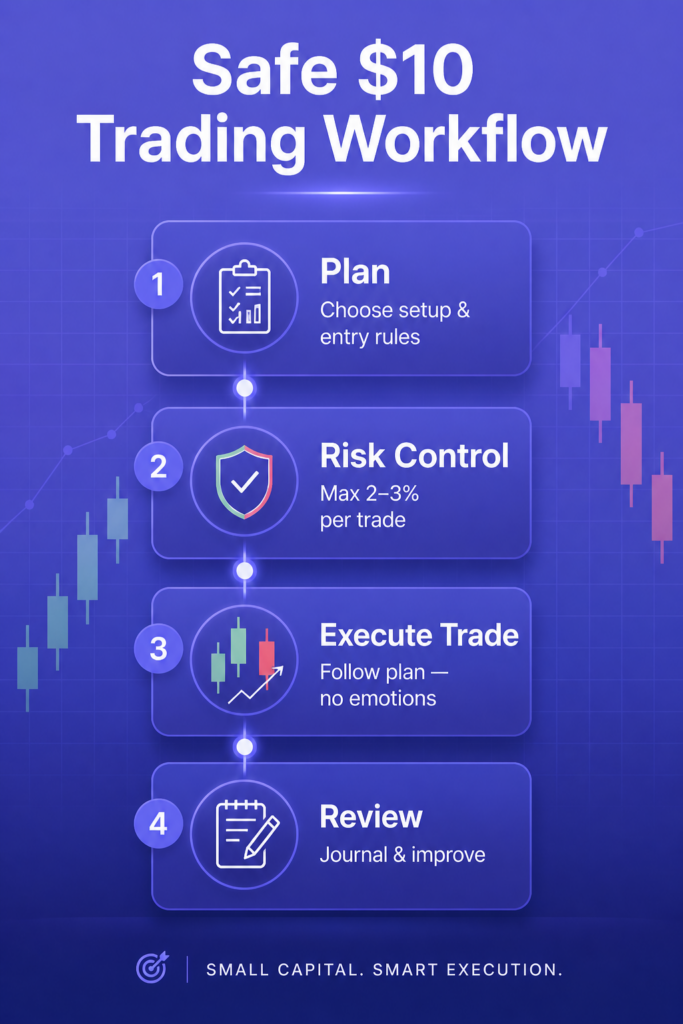

You can start with $10 on Deriv, but whether you can survive, learn, and grow that account depends entirely on your expectations, discipline, and strategy.

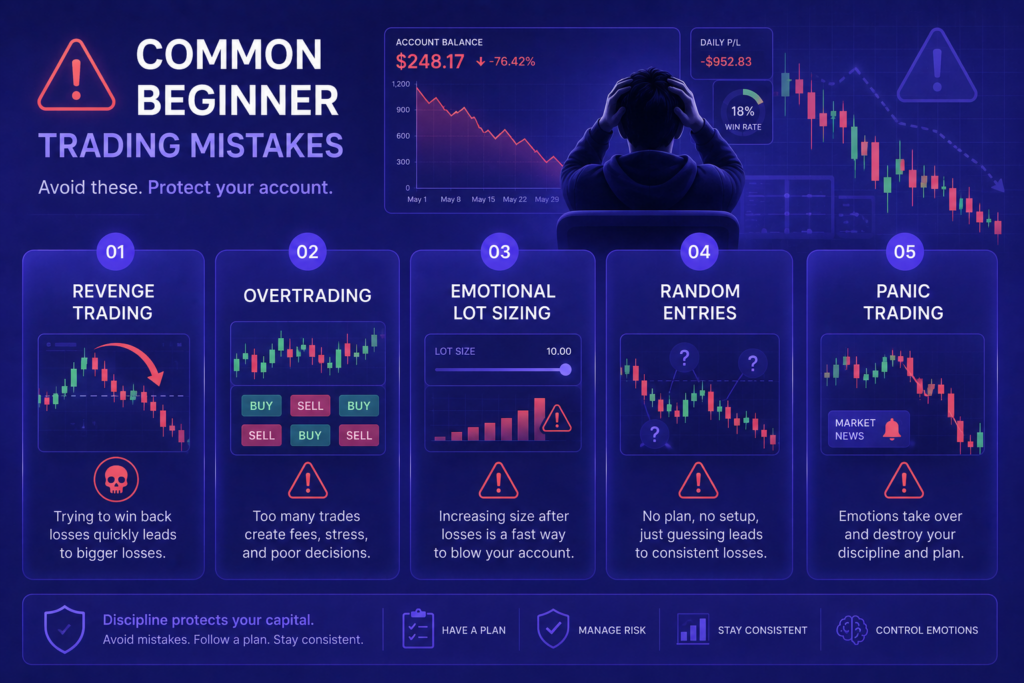

Most beginners lose their first small deposit because they treat trading like gambling. They overtrade, chase losses, and use unrealistic position sizes. The platform itself is not usually the problem. The lack of structure is.

In this guide, I’ll break down:

Whether $10 is truly enough

What trading styles work with tiny balances

Which platforms are better for low deposits

The mistakes that destroy small accounts

Realistic income expectations

How to build consistency slowly instead of blowing accounts repeatedly

If you are completely new to trading, you should first read this beginner-focused guide on the realistic amount of money needed to start trading because most social media influencers give completely unrealistic expectations.

Is $10 Enough to Start Trading on Deriv?

Technically, yes.

Practically, it depends on how you trade.

Deriv allows very small position sizes, especially on synthetic indices and certain CFD products. That flexibility is one reason many beginners use it.

The main advantage of starting with $10 is not profit potential.

It is survival.

A small deposit lets beginners:

Learn platform mechanics

Understand emotional control

Practice risk management

Experience real market pressure

Avoid losing large amounts early

This is why many experienced traders recommend starting tiny rather than depositing hundreds immediately.

But there’s a major problem.

Most people expect a $10 account to become $1,000 quickly.

That mindset destroys accounts faster than bad strategies.

What Happens to Most $10 Accounts?

Most small accounts die because of one thing:

Overleveraging.

A beginner sees a small balance and thinks:

“I need to grow this fast.”

So they increase trade size aggressively.

One bad trade suddenly wipes out 20% to 50% of the account.

Final Verdict: Can You Really Start Trading with $10 on Deriv?

Yes.

You absolutely can.

But success depends less on the platform and more on your mindset.

A $10 account should be treated as:

A learning phase

A discipline-building phase

A psychology training phase

A risk-management practice account

Most beginners fail because they expect instant income.

The traders who survive long term usually think differently.

They focus on:

Consistency

Patience

Controlled risk

Emotional stability

Long-term growth

That is the real edge in trading.

And that is exactly why many traders eventually join communities focused on deeper analysis and structured learning instead of random signal chasing.

If you want serious market breakdowns, disciplined trading insights, and deeper strategy analysis beyond basic beginner content, you can explore the BECoin Premium Membership.

Which Broker Has the Cleanest Interface? Real Comparison for Beginners in 2026

Looking for the cleanest trading interface in 2026? Compare Binomo, IQ Option, Quotex, Deriv, and more based on speed, layout, usability, mobile experience, and beginner friendliness.

When most beginners choose a broker, they focus on bonuses, payouts, or deposit methods. But after testing multiple platforms for months, I realized something surprising:

A messy interface can destroy your trading faster than a bad strategy.

Too many flashing indicators, confusing dashboards, cluttered chart tools, and distracting layouts create emotional trading. Meanwhile, a clean interface helps you stay calm, focused, and disciplined.

That matters far more than most traders realize.

In this guide, I tested some of the most popular trading platforms and compared them purely based on interface quality, usability, chart experience, speed, mobile optimization, and beginner friendliness.

This is based on real usability experience, not marketing hype.

Why Interface Quality Matters More Than Beginners Think

Most new traders underestimate how much platform design affects decision making.

A clean interface helps you:

Focus on entries instead of distractions

Avoid accidental trades

Read candles faster

Control emotions better

Execute trades quickly during volatility

Learn faster as a beginner

A cluttered platform creates confusion, especially during fast market movement.

Deriv offers one of the most feature-rich ecosystems.

But clean interface?

Not always.

The platform includes multiple systems, dashboards, and trading modes. That gives experienced traders flexibility, but beginners may initially struggle.

The synthetic indices environment especially feels more technical compared to Binomo or Quotex.

That said, experienced traders often appreciate Deriv because the complexity comes with more control.

If you truly want an edge beyond platform design, BeCoin Premium is where strategy matters more than hype.

Safest Broker for Small Deposits in 2026

Looking for the safest broker for small deposits in 2026? Discover beginner-friendly trading platforms with low minimum deposits, reliable withdrawals, risk controls, and the best options for starting safely with limited capital.

Starting trading with a small amount of money sounds easy until you actually deposit real funds. Most beginners quickly realize that choosing the wrong broker can wipe out a small account before they even learn the basics.

That is why safety matters far more when your deposit is small.

If you start with $10, $20, or even $50, every mistake becomes expensive. High fees, delayed withdrawals, aggressive trading conditions, poor execution, and emotional pressure can destroy small accounts very fast.

After testing multiple brokers, checking withdrawal experiences, platform stability, beginner tools, and small account usability, I found that the safest broker for small deposits is not necessarily the one with the biggest marketing campaigns.

The safest broker is the one that helps beginners survive long enough to actually learn.

Many beginners think “safe” simply means regulated.

That matters, but for small deposit traders, practical safety is even more important.

A safe broker for a $10 or $20 trader should provide:

Low minimum deposit

Stable order execution

Fast and consistent withdrawals

Beginner-friendly interface

Risk management tools

Low emotional pressure

Mobile optimization

Low lag on weak internet

Clear KYC system

Reasonable payout structure

Small account traders are extremely vulnerable to emotional trading. That is why broker design matters.

Some brokers push traders toward overtrading through flashy interfaces, aggressive tournaments, and unrealistic expectations. Others provide a calmer environment that helps beginners survive longer.

You should also understand that no broker guarantees profits. Even the safest platform cannot protect traders from poor risk management.

Choosing the safest broker for small deposits is ultimately about reducing unnecessary risk while building real trading experience.

Beginners often waste months chasing unrealistic profits instead of focusing on consistency and discipline.

The brokers listed in this guide each have strengths for smaller accounts, but none of them replace proper psychology and risk management.

A safe trading journey usually looks like this:

Start small

Learn slowly

Control emotions

Protect capital

Build consistency

Scale gradually

That approach may sound boring compared to social media trading hype, but it is far more sustainable.

The traders who survive long enough to become profitable are usually the ones who stop trying to get rich overnight.

They focus on protecting their account first.

Everything else comes later.

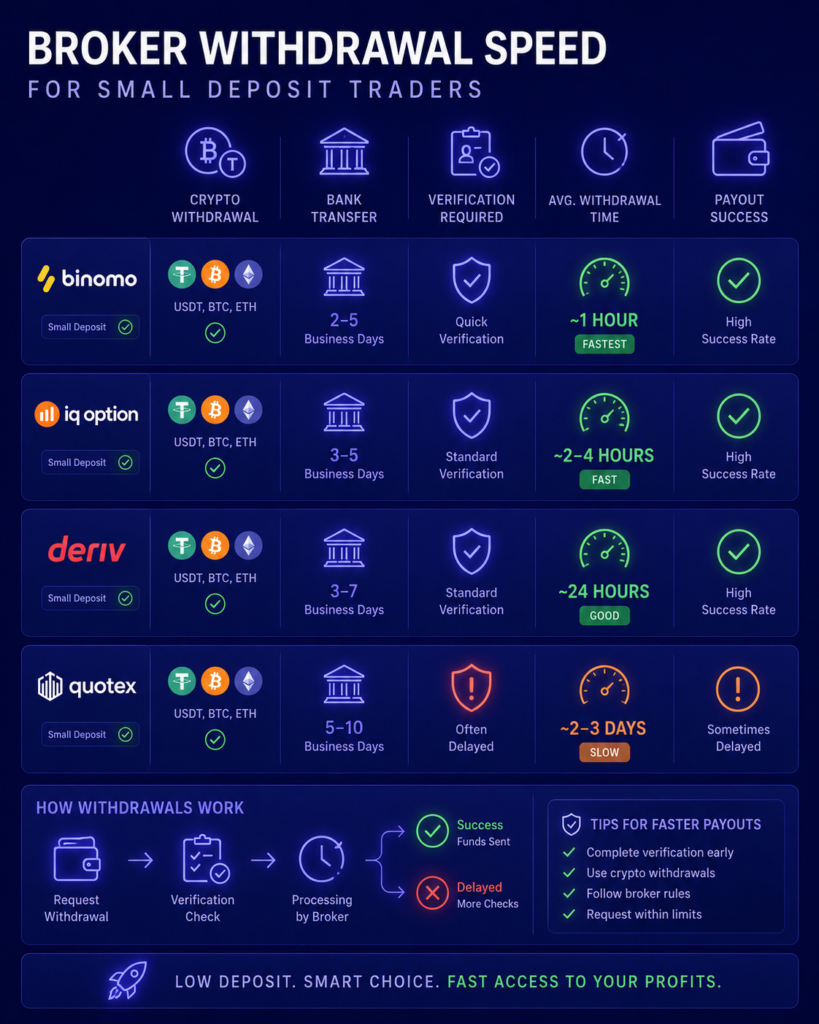

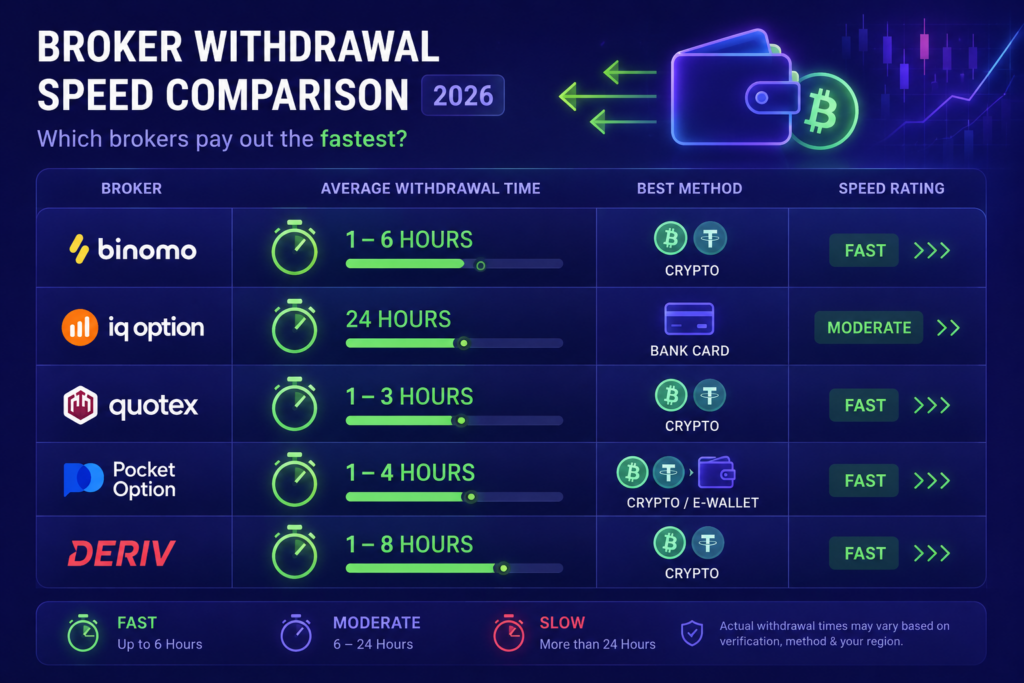

Which Broker Has Faster Withdrawals? Real 2026 Comparison for Traders

When most beginners choose a broker, they focus on bonuses, signals, or flashy interfaces.

But after trading for a while, you realize one thing matters more than almost anything else:

How fast can you actually withdraw your money?

A broker can look perfect until your first withdrawal request gets stuck in “processing” for three days. That is where the real difference between platforms becomes obvious.

In this guide, I compared some of the most popular trading brokers based on actual withdrawal speed, payout consistency, verification requirements, payment methods, and user experience. This is especially important for small account traders, students, and traders in countries where banking systems are slower.

Why Withdrawal Speed Matters More Than Most Beginners Think

Fast withdrawals are not just about convenience.

They affect your psychology, trust in the platform, and even your risk management.

When traders know they can withdraw profits quickly, they usually trade more calmly and avoid emotional overtrading. Slow withdrawals create anxiety, revenge trading, and poor decision-making.

Bank cards and e-wallets often depend on regional banking systems.

Withdrawal Amount

Small withdrawals usually process faster than large ones because large transactions often trigger manual reviews.

Country Restrictions

Some regions experience delays because of local banking systems or payment provider limitations.

This is especially relevant for traders in Pakistan and similar regions. You can also explore Best Broker for Pakistani Traders in 2026 for region-specific platform comparisons.

Which Brokers Usually Process Withdrawals the Fastest?

Here is a realistic overview based on trader feedback, platform testing, and common user experiences.

Binomo is popular among beginner traders because of its simple interface and relatively fast withdrawal system for verified users.

In many cases, smaller withdrawals through e-wallets or crypto are processed within a few hours. Larger withdrawals may take longer depending on account verification status.

One thing I noticed with Binomo is that the platform performs better once your account is fully verified before requesting withdrawals. Traders who skip verification often experience delays later.

If you are comparing the platform directly against IQ Option, these guides will help:

IQ Option remains one of the most recognized trading platforms globally.

Its withdrawal system is generally reliable, but processing speed depends heavily on payment method and region.

Crypto withdrawals are usually faster than bank cards. Some traders receive funds within hours, while others wait one to three business days.

One advantage of IQ Option is its smoother banking integration in many countries. However, verification checks can become stricter for larger accounts.

If you want a broader beginner comparison involving IQ Option, read:

Final Verdict: Which Broker Has Faster Withdrawals?

If we focus purely on average withdrawal speed for most users:

Crypto-friendly brokers usually process fastest.

Platforms like Quotex, Pocket Option, Deriv, and Binomo often deliver quicker payouts compared to traditional bank-card-focused systems.

However, the “best” broker depends on your country, payment method, and trading style.

For beginners, reliability matters more than chasing the absolute fastest payout claim.

A slightly slower broker with stable withdrawals is far better than a platform with flashy promises and inconsistent payments.

Want an Edge Beyond Just Choosing the Right Broker?

Most traders spend too much time searching for the perfect platform and not enough time improving their strategy.

The reality is simple:

Even the fastest withdrawal broker cannot save poor risk management or emotional trading.

That is why serious traders focus on market understanding, consistency, and disciplined execution.

If you want deeper trading analysis, smarter trade planning, premium educational content, and a more structured approach to trading, check out Becoin Premium Membership.

The goal is not just faster withdrawals.

The real goal is building consistent trading habits that actually grow your account over time.

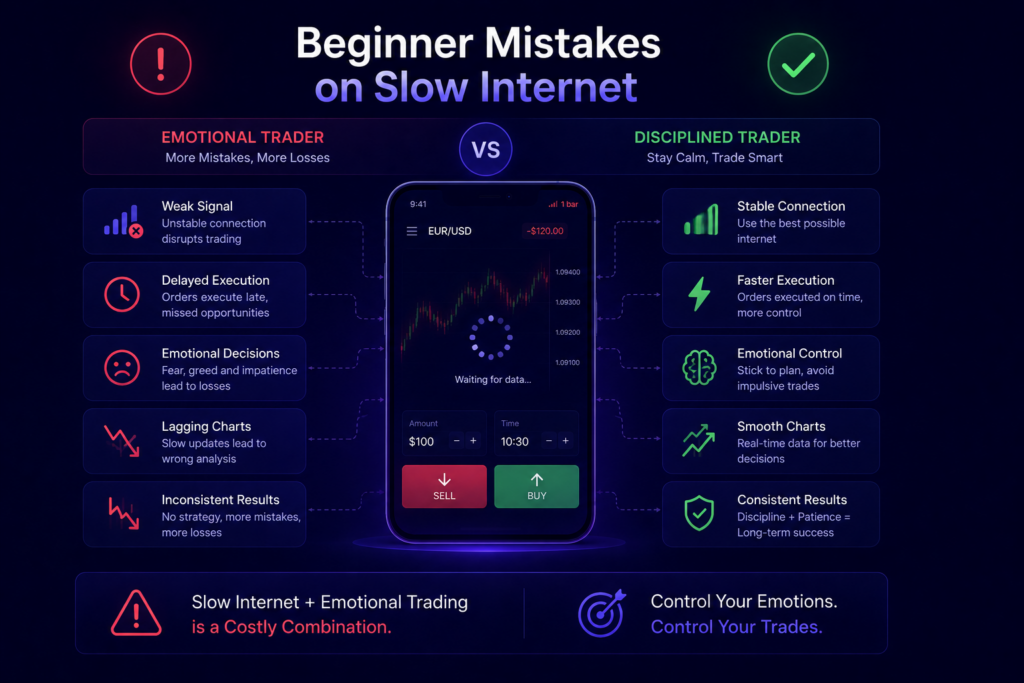

Best Trading Platform for Slow Internet in 2026

A slow internet connection can ruin trades faster than a bad strategy.

Charts freeze, apps reload, and delayed execution creates unnecessary losses. This is especially common for traders using mobile data, shared WiFi, or older smartphones.

Most broker reviews ignore this issue completely.

After testing multiple platforms on weaker connections and low-end Android devices, some brokers clearly handled slow internet much better than others.

In this guide, you will discover:

Which platforms run smoothly on weak internet

Which apps use fewer phone resources

Which brokers reconnect faster after signal drops

Which platform is best for beginners using mobile data

What Makes a Trading Platform Good for Slow Internet?

A good low-bandwidth trading platform should:

Load charts quickly

Use lightweight app design

Handle reconnections smoothly

Avoid freezing during trades

Work properly on older phones

Consume less mobile data

Heavy animations and overloaded dashboards often create lag during volatile markets.

That is why lightweight platforms usually perform better for beginners.

1. Binomo

Binomo is one of the smoothest trading platforms for slow internet users.

The app is lightweight, responsive, and performs well even on weaker Android devices. During testing on unstable mobile data, chart loading and reconnection speed were better than most competitors.

Why Binomo Works Well on Slow Internet

Lightweight mobile app

Stable execution on weak networks

Beginner-friendly interface

Lower RAM and battery usage

Smooth chart loading

Drawback

Advanced traders may find the charting tools limited compared to IQ Option.

IQ Option offers one of the best charting experiences in the industry.

The platform feels more premium and advanced than most beginner brokers. However, it also consumes more device resources.

On the strong internet, IQ Option performs excellently. On weaker connections, low-end phones may experience occasional lag during volatile market conditions.

Why Traders Still Prefer IQ Option

Excellent chart quality

Professional interface

Better analysis tools

Strong mobile app optimization

Drawback

The app is heavier than Binomo and may use more mobile data.

The goal is making better decisions with better discipline and consistency.

Deriv vs IQ Option for Synthetic Indices: Which Platform Is Better in 2026?

Synthetic indices have become one of the most talked about trading categories among beginners and experienced traders alike. Unlike forex or crypto markets that depend on real world events, synthetic indices operate 24/7 using algorithm driven price movements. That means traders can access opportunities at any time without waiting for market openings or major news events.

But one question keeps coming up repeatedly:

Should you trade synthetic indices on Deriv or IQ Option?

After spending time testing both platforms, comparing execution speed, chart quality, payout structures, risk management tools, mobile usability, and overall trading experience, the answer is not as simple as choosing the platform with the highest payout.

Both platforms target different types of traders.

Deriv is heavily focused on synthetic indices and volatility trading. IQ Option, on the other hand, provides a more polished all in one trading environment with cleaner charts and beginner friendly tools.

This guide breaks down everything you actually need to know before choosing between them.

You will also discover which broker works better for beginners, which one is safer for low budget traders, and why most traders fail when trading synthetic indices.

If you are completely new to trading, start with this guide first:

Synthetic indices are simulated markets generated by algorithms instead of real market assets like stocks, currencies, or commodities.

The biggest reason traders like them is consistency.

Traditional markets can become slow or unpredictable depending on news events, market sessions, and liquidity. Synthetic indices continue running continuously with controlled volatility patterns.

Deriv became popular mainly because of its Volatility Indices, Crash and Boom markets, and Jump Indices.

These indices mimic real market behavior but are not connected to actual economic events.

For many traders, especially in countries where forex access is limited or unstable, synthetic indices offer a simple way to practice strategy execution without worrying about political announcements or market closures.

However, synthetic indices are also dangerous for emotional traders.

Fast price movement combined with leverage can destroy accounts quickly if risk management is weak.

Deriv dominates the synthetic indices space for one major reason.

The platform was designed around it.

Most traders who specifically want to trade Volatility 75, Boom and Crash, or Jump Indices eventually end up on Deriv because these instruments are deeply integrated into the trading environment.

What Makes Deriv Strong?

Deriv gives traders access to:

Volatility Indices

Crash and Boom indices

Jump indices

Range break indices

Multipliers

Automated trading support

MT5 compatibility

The biggest advantage is flexibility.

You can scalp aggressively, hold longer trades, automate strategies, or build technical systems around volatility behavior.

For advanced traders, this matters a lot.

Another major strength is continuous market access. Since synthetic indices operate 24/7, traders are not restricted by market sessions.

This is especially useful for students and part time traders.

If you are trading on a very small budget, you should also read:

Is Deriv better than IQ Option for synthetic indices?

Yes, Deriv is generally better for synthetic indices because the platform is specifically built around volatility and synthetic trading products.

Can beginners trade synthetic indices?

Yes, but beginners should start with demo accounts and strict risk management because synthetic indices can move aggressively.

Which platform is easier to use?

IQ Option is easier for beginners because of its cleaner interface and simpler trading environment.

Are synthetic indices available on IQ Option?

IQ Option offers some synthetic style trading opportunities, but it does not provide the same specialized synthetic ecosystem available on Deriv.

What is the safest way to start trading synthetic indices?

The safest approach is starting with small position sizes, demo trading, and strong risk management rules.

Best Broker for One Trade a Day Strategy in 2026

Most traders lose money because they trade too much.

They enter random setups, chase candles, overreact emotionally, and turn a simple strategy into pure gambling. That is exactly why the one trade a day strategy is becoming more popular among smart traders in 2026.

Instead of sitting in front of charts all day, this approach focuses on patience, quality setups, controlled risk, and emotional discipline.

You wait. You analyze. You take one clean trade. Then you stop.

Sounds simple, but the broker you choose matters a lot.

A bad platform can ruin this strategy through laggy execution, delayed withdrawals, confusing interfaces, or emotional distractions. A good broker helps you stay focused and disciplined.

In this guide, we will break down the best brokers for one trade a day trading strategies, compare their strengths, explain who they are best for, and help you choose the right platform depending on your experience level.

The biggest advantage of this strategy is psychological control.

Most beginner traders lose because they overtrade. One loss turns into revenge trading. One small win turns into greed. Suddenly, five random trades appear within an hour.

The one trade a day method removes most emotional mistakes.

You focus on:

Higher quality setups

Better risk management

Less emotional pressure

More consistent decision making

Long term account survival

This approach works especially well for:

Students

Part time traders

People with jobs

Traders with small accounts

Beginners learning discipline

If you struggle with overtrading, read Why 90% of Traders Lose Money because it explains the exact psychological traps most traders never notice.

What Makes a Broker Good for One Trade a Day?

A one trade a day strategy requires a different mindset compared to high frequency trading.

You do not need hundreds of indicators or advanced tools.

You need:

Fast and Stable Execution

If your trade enters late, your entire setup can fail.

Simple and Clean Interface

Too much noise creates emotional trading.

Fast Withdrawals

Reliable withdrawals help traders trust the platform and avoid emotional panic.

Good Mobile Experience

Many traders using this strategy analyze markets during work breaks or study sessions.

Low Deposit Flexibility

Since this strategy focuses on consistency, many traders start small.

Binomo remains one of the easiest platforms for disciplined beginner traders.

The interface is extremely clean, which helps reduce emotional distractions. For traders using one high quality setup daily, this simplicity becomes a major advantage.

The platform works well for:

New traders

Small account users

Mobile focused traders

Students

Traders practicing discipline

One of Binomo’s biggest strengths is its beginner friendly environment. It does not overwhelm users with unnecessary complexity.

The mobile app is smooth, execution is stable, and the platform is easy to learn even if you have never traded before.

For traders trying to build patience and consistency, that simplicity matters.

IQ Option is one of the strongest platforms for traders who want better charting tools and deeper technical analysis.

If your one trade a day strategy depends heavily on support and resistance, trend analysis, candlestick confirmations, or indicators, IQ Option provides a stronger analytical environment.

The platform feels more advanced compared to Binomo.

That makes it ideal for:

Intermediate traders

Technical analysis focused traders

Strategy based traders

Traders who prefer detailed charts

The interface still remains beginner friendly enough for newer users, but the analytical tools are clearly more advanced.

A disciplined trader with proper analysis will always outperform emotional traders chasing random entries all day.

That is exactly why the one trade a day strategy continues to work in 2026.

Which Broker Is Better for Students in 2026?

For students, trading usually starts with one simple goal: learning how markets work without risking too much money.

Most students are not starting with huge budgets. They are trading from a phone, using mobile internet, balancing studies, and trying to avoid losing money quickly. That changes what actually matters in a broker.

The “best broker” for a student is not necessarily the one with the biggest features or advanced tools. It is the one that feels easier to learn, works smoothly on mobile, allows small deposits, and helps beginners practice without getting overwhelmed.

Some platforms focus on simplicity. Others offer deeper analysis tools. Some are better for low risk learning while others suit faster traders.

In this guide, we will compare the most popular brokers students use in 2026 and help you understand which one may fit your trading style best.

Binomo remains popular among students because of its simple design and beginner friendly layout.

The platform is easier to understand compared to many advanced brokers. New traders can quickly learn how entries, expiry times, and risk management work without spending weeks learning technical systems.

The mobile app also performs smoothly on lower end Android devices, which makes it practical for students.

Why Many Students Prefer Binomo

Very beginner friendly interface

Low starting deposit

Easy mobile trading experience

Fast learning curve

Clean chart layout

Students who struggle with emotional trading should also read why 90% of traders lose money because psychology becomes even more important when trading with small balances.

Potential Downsides

Binomo is simpler than some competitors. That helps beginners, but advanced traders may later want more technical tools and deeper analysis features.

Most student traders fail because they rely on random entries, copied signals, and emotional decisions.

At BeCoin Premium, the focus is different.

You get:

In depth market analysis

Higher quality trade setups

Better risk management insights

Educational guidance for long term growth

Structured learning instead of gambling style trading

If you want to improve your trading decisions and develop real consistency, you can join BeCoin Premium here.

Best Broker for Pakistani Traders in 2026

Finding the best broker in Pakistan is not as simple as choosing the platform with the biggest ads or the highest payout percentage. Pakistani traders face unique challenges including payment method limitations, withdrawal delays, unstable strategies, and brokers that look attractive at first but become difficult to use later.

Many beginners deposit money into the wrong platform, use high risk trading styles, and lose their balance before understanding how the market works. The broker you choose directly affects your trading speed, execution quality, withdrawal experience, and long term consistency.

In this guide, we will compare the most popular brokers used by Pakistani traders in 2026 including Binomo, IQ Option, Deriv, Quotex, ExpertOption, Olymp Trade, and CapitalCore. We will also explain which broker works best for beginners, low budget traders, mobile users, and traders looking for fast withdrawals.

Why Broker Selection Matters More Than Most Beginners Realize

Most traders focus only on signals and strategies. But even a strong strategy can fail on a bad platform. Common broker problems Pakistani traders face include:

Delayed withdrawals

Lag during volatile market conditions

Limited deposit methods

High minimum deposits

Poor mobile apps

Unstable execution speed

Emotional overtrading due to poor interface design

A reliable broker should make trading smoother, not harder.

Binomo remains one of the most beginner friendly brokers for Pakistani traders in 2026. The platform is simple, lightweight, and works smoothly even on low end smartphones and slower internet connections.

The biggest advantage of Binomo is simplicity. Many beginners become overwhelmed by complicated dashboards and advanced charting tools. Binomo removes much of that confusion and allows traders to focus on entries, timing, and risk management.

It is especially popular among traders starting with small balances.

Why Pakistani Traders Like Binomo

Easy interface for beginners

Small deposit friendly

Fast trade execution

Smooth Android experience

Lower learning curve compared to complex platforms

IQ Option is ideal for traders who want advanced charting, technical indicators, and a more professional trading environment.

The platform offers stronger analytical tools than most beginner focused brokers. Traders who already understand support and resistance, trend structure, or candlestick patterns usually prefer IQ Option over simpler alternatives.

Best Features of IQ Option

Advanced charting tools

Multiple indicators

Strong mobile application

Better for technical analysis

Smooth market switching

However, beginners sometimes overcomplicate their trading because the platform offers too many tools.

Quotex has become extremely popular because of its clean interface and fast execution.

Many traders moving from cluttered platforms prefer Quotex because it reduces distractions. The chart area feels cleaner, which helps traders focus more on price action.

Quotex is especially attractive for short session trading and mobile users.

ExpertOption focuses heavily on fast execution and quick trading sessions. The interface feels modern and responsive, though some traders eventually move toward platforms with stronger analytical features.

CapitalCore attracts traders interested in higher leverage style environments and alternative trading conditions. It is more suitable for users who already understand risk management.

You should also understand the truth behind no KYC brokers.

Final Verdict: Best Broker for Pakistani Traders

There is no perfect broker for everyone.

For beginners and small balances, Binomo and Quotex are easier to start with.

For advanced chart analysis, IQ Option is stronger.

For flexible markets and long term trading growth, Deriv offers more possibilities.

The most important thing is not choosing the broker with the biggest promises. It is choosing the platform that matches your experience level, trading psychology, and risk tolerance.

Most traders fail because they chase fast profits without building a structured trading process.

Want an Edge Over Most Traders?

Using a good broker is only the first step. Real consistency comes from understanding market structure, multi timeframe analysis, entry timing, and disciplined execution.

If you want deeper market analysis, smarter trade planning, and a more structured trading approach, join Becoin Premium here.

Binomo vs IQ Option Mobile App Comparison 2026: Which Trading App Is Better for Beginners?

Mobile trading is no longer a backup option for traders. For many beginners, the smartphone app becomes the main trading workstation. Whether you are entering quick trades during a lunch break or analyzing charts late at night, the quality of a broker’s mobile app can directly impact your results.

Two platforms that continue to dominate beginner-focused trading discussions are Binomo and IQ Option. Both offer mobile apps with fast execution, chart tools, and low deposit requirements, but their overall trading experience feels very different once you start using them daily.

In this detailed comparison, we will break down everything from app performance and charting quality to execution speed, indicators, risk management, and beginner usability.

The Binomo app focuses heavily on simplicity. The interface is clean, lightweight, and designed for fast trade execution. Beginners usually adapt to it quickly because the learning curve is smaller.

Key strengths include:

Easy navigation

Fast order placement

Lightweight app performance

Beginner-friendly trade layout

Simple deposit and withdrawal system

The platform is especially popular among traders using smaller accounts or short trading sessions.

IQ Option offers a more advanced trading environment. The app includes richer charting features, more technical indicators, and deeper customization options. Traders who want a professional-style interface often prefer it.

Key strengths include:

Advanced charting system

More indicators and tools

Better customization

Multi-asset support

Strong visual trading interface

The app feels closer to a desktop trading terminal compared to Binomo’s simplified design.

Binomo’s biggest strength is speed and simplicity. Even someone completely new to trading can understand the interface within minutes.

The trading buttons are large and clear. Switching assets is simple. The chart area does not feel overcrowded. This matters because many beginners make mistakes when using overly complicated interfaces.

The mobile app also performs smoothly on lower-end Android devices, which is important for traders in regions where premium smartphones are less common.

Binomo and IQ Option both offer strong mobile trading experiences, but they target slightly different trader personalities.

Binomo is better for simplicity, fast execution, and beginner comfort.

IQ Option is better for advanced charting, deeper technical analysis, and long-term analytical development.

Most beginners initially prefer Binomo because it feels easier and less intimidating. However, traders who become serious about technical analysis often migrate toward IQ Option later.

The smartest approach is not just choosing the better app. It is learning how to manage risk, analyze multiple timeframes, and avoid emotional trading mistakes.

For traders who want a real edge with deeper market structure analysis, multiple timeframe confirmations, and smarter trading discipline, explore BeCoin Premium Trading Plans.

FAQs

Is Binomo mobile app good for beginners?

Yes. Binomo is considered beginner-friendly because of its clean interface, lightweight design, and fast trade execution.

Does IQ Option have better charting tools than Binomo?

Yes. IQ Option generally offers more advanced indicators, chart customization, and technical analysis features.

Which app works better on low-end phones?

Binomo usually performs better on weaker Android devices because the app is lighter and simpler.

Can you trade professionally using mobile apps?

Yes, but professional trading still requires risk management, strategy discipline, and proper analysis. The app alone does not guarantee profitability.

Which app is safer for small account trading?

Both platforms can be used with small accounts, but risk management matters more than the platform itself. Beginners should focus on low-risk position sizing and emotional discipline.

Deriv vs Binomo for Low-Risk Trading in 2026: Which Platform Is Better for Safer Growth?

Most beginners enter trading with one simple goal: avoid blowing up their account in the first week.

That is exactly why low-risk trading matters more than fast profits.

Two platforms that constantly appear in beginner discussions are Deriv and Binomo. Both allow small deposits, short-term trading, and beginner-friendly access. But when your focus is protecting capital instead of gambling for quick wins, the differences between them become much more important.

Some traders prefer Deriv because of its flexible risk management tools and multiple trading markets. Others prefer Binomo because of its simpler interface and lower learning curve.

The real question is this:

Which platform actually supports low-risk trading better in 2026?

In this guide, we will compare both brokers from a realistic beginner perspective, including:

Risk control features

Small account management

Demo trading quality

Emotional pressure during trading

Withdrawal reliability

Strategy flexibility

Long-term sustainability

If your goal is steady growth instead of emotional overtrading, this comparison will help you make the right choice.

Understanding Low-Risk Trading First

Low-risk trading does not mean “no losses.”

It means structuring trades in a way that protects your account from major damage.

A low-risk trading platform should help traders stay disciplined instead of encouraging impulsive behavior.

That includes:

Better chart visibility

Flexible trade sizing

Stable execution

Reliable withdrawals

Lower emotional pressure

Strategy testing tools

Multi-timeframe analysis support

This is where Deriv and Binomo begin to separate.

Deriv vs Binomo: Quick Overview

Feature

Deriv

Binomo

Minimum Deposit

Very low

Very low

Trading Types

Forex, synthetic indices, multipliers, options

Fixed time trading

Risk Flexibility

High

Moderate

Beginner Simplicity

Medium

Very High

Multi-Timeframe Analysis

Strong

Limited

Strategy Depth

Advanced

Basic to Intermediate

Emotional Trading Risk

Lower with proper setup

Higher for impulsive traders

Demo Account

Excellent

Good

Long-Term Scalability

Strong

Moderate

Why Many Low-Risk Traders Prefer Deriv

Deriv has evolved far beyond simple binary-style trading.

The platform now offers multiple trading environments, including synthetic indices, forex CFDs, multipliers, and options trading.

For low-risk traders, the biggest advantage is flexibility.

Instead of forcing traders into short expiration trades constantly, Deriv allows better control over:

Stop losses

Position sizing

Trade duration

Market selection

Risk-to-reward planning

This creates a calmer trading environment overall.

A beginner who learns patience on Deriv usually survives longer than someone constantly chasing fast entries.

Another major advantage is multi-timeframe chart analysis. Traders can combine higher timeframe direction with lower timeframe entries, reducing random trades significantly.

That matters because low-risk trading is often more about avoiding bad trades than finding perfect trades.

Binomo’s Strength for New Traders

Binomo remains extremely popular among beginners because it is easy to understand.

The interface is simple.

The execution process is straightforward.

A new trader can open an account and start demo trading within minutes.

For some people, this simplicity reduces confusion and helps them focus on discipline instead of technical complexity.

Binomo also works well for traders who prefer short sessions and quick setups.

However, there is a downside.

The simplicity can sometimes encourage impulsive behavior.

Fast-entry environments often create emotional trading habits, especially for beginners chasing rapid profits.

This becomes dangerous for small accounts.

If you are trading emotionally, even a few bad sessions can destroy weeks of progress.

That is why many traders eventually transition toward platforms with deeper analysis capabilities.

If your main priority is long-term survival and lower-risk trading, Deriv usually offers the stronger environment.

The platform gives traders more flexibility, deeper analysis tools, and better scalability over time.

Binomo still works well for absolute beginners who want simplicity and a cleaner learning curve.

But simplicity alone does not guarantee profitability.

Eventually, serious traders need stronger analysis systems and better risk control.

That is why many traders start simple and later transition toward more advanced structures.

Start With the Right Platform

If you want a more flexible trading environment with better long-term growth potential, you can start with Deriv and test strategies safely on demo before risking real capital.

If you prefer a beginner-friendly interface with faster learning simplicity, many traders also explore IQ Option alongside Binomo for comparison before choosing their primary platform.

Final Verdict

Low-risk trading is not about finding a magic indicator.

It is about building a system that protects your capital while improving your decision-making over time.

Deriv generally provides better tools for that process.

Binomo provides easier access for beginners.

The best traders eventually combine:

Patience

Risk management

Multi-timeframe analysis

Emotional control

Consistency

That is exactly why many developing traders join Becoin Premium to gain access to deeper multi-timeframe analysis, structured trading insights, and higher-quality market breakdowns designed to help traders avoid emotional mistakes and improve long-term consistency.

FAQs

Is Deriv safer for low-risk trading than Binomo?

For most disciplined traders, yes. Deriv offers better flexibility for risk management, trade planning, and multi-timeframe analysis.

Is Binomo good for beginners?

Yes. Binomo is easier to understand initially and works well for traders who want a simpler interface.

Can I start trading with a small budget on both platforms?

Yes. Both platforms support small deposits, but proper risk management is still essential.

Which platform is better for long-term trading growth?

Deriv generally offers better long-term scalability because of its wider markets and stronger analytical tools.

Do professional traders use multi-timeframe analysis?

Yes. Multi-timeframe analysis is one of the most common methods used to reduce low-quality entries and improve trade timing.

Deriv vs IQ Option for Beginners in 2026: Which Platform Is Better to Start With?

Choosing your first trading platform can decide whether you stay consistent or quit after blowing your first account.

Most beginners do not fail because trading is impossible. They fail because they start on platforms that confuse them, encourage emotional trading, or make risk management difficult.

Two names that often appear in beginner discussions are Deriv and IQ Option.

Both platforms are popular among new traders because they allow small deposits, offer demo accounts, and have relatively simple interfaces. But they are built differently, and that difference matters a lot when you are starting with limited capital.

This guide compares Deriv and IQ Option from a real beginner perspective, including:

Ease of use

Deposit requirements

Charting experience

Risk management

Withdrawals

Strategy flexibility

Emotional trading risks

Long term learning potential

If you are completely new to trading, this comparison will help you avoid common beginner mistakes and choose the platform that actually fits your goals.

Deriv is a multi-asset trading platform that offers forex, synthetic indices, multipliers, CFDs, and options trading.

One reason many beginners choose Deriv is flexibility. You can start with very small amounts and access different trading styles without needing multiple broker accounts.

Deriv also offers several platforms inside one ecosystem, including:

DTrader

Deriv MT5

SmartTrader

Deriv X

For beginners, this flexibility can either be a huge advantage or slightly overwhelming depending on how fast they want to learn.

If you want a broker that gives you room to grow beyond basic beginner trading, Deriv is a strong option.

IQ Option became extremely popular because of its clean interface and beginner friendly design.

The platform focuses heavily on simplicity. New traders can quickly open charts, place trades, and understand basic market movement without dealing with too many advanced settings.

For many beginners, IQ Option feels less intimidating compared to platforms like MT5.

It is especially popular among traders who:

Start with small deposits

Prefer short term trading

Want a smooth mobile experience

Need simple chart tools

Learn visually rather than technically

If your goal is to learn trading gradually without too much complexity, IQ Option can feel easier during the first few weeks.

The interface is clean, modern, and beginner focused. Everything is visually organized, and even someone with zero trading experience can understand the basics quickly.

Charts are responsive, indicators are easy to add, and placing trades takes only a few clicks.

Deriv, on the other hand, gives you more flexibility and tools. But because of that, beginners may initially feel overwhelmed.

For example:

Multiple platform choices

More instrument categories

Advanced chart customization

Different trading modes

If you only want the easiest possible entry into trading, IQ Option usually wins here.

But if you plan to grow into forex, CFDs, or advanced technical analysis later, Deriv offers more room for progression.

Quick Beginner Recommendation

If you want simplicity and a smoother beginner experience:

Instead of gambling on random entries, you learn how experienced traders actually analyze the market before taking trades.

Binomo vs IQ Option Withdrawal Speed: Full 2026 Comparison Guide

Withdrawal speed is one of the most important factors for traders, especially beginners who want quick access to profits. A platform may look good for trading, but if getting your money takes too long, frustration builds fast.

In this detailed comparison of Binomo and IQ Option, we will break down real withdrawal timelines, processing behavior, payment methods, and hidden factors that affect how quickly you actually receive your funds.

Why Withdrawal Speed Matters in Trading

Fast withdrawals are not just convenience. They directly affect trust, risk management, and reinvestment strategy.

Traders often underestimate this point:

Slow withdrawals reduce confidence in a platform

Fast payouts allow quicker compounding of profits

Delays can indicate verification or liquidity issues

Payment method selection can change timing significantly

If your goal is consistent trading growth, withdrawal speed is as important as entry accuracy.

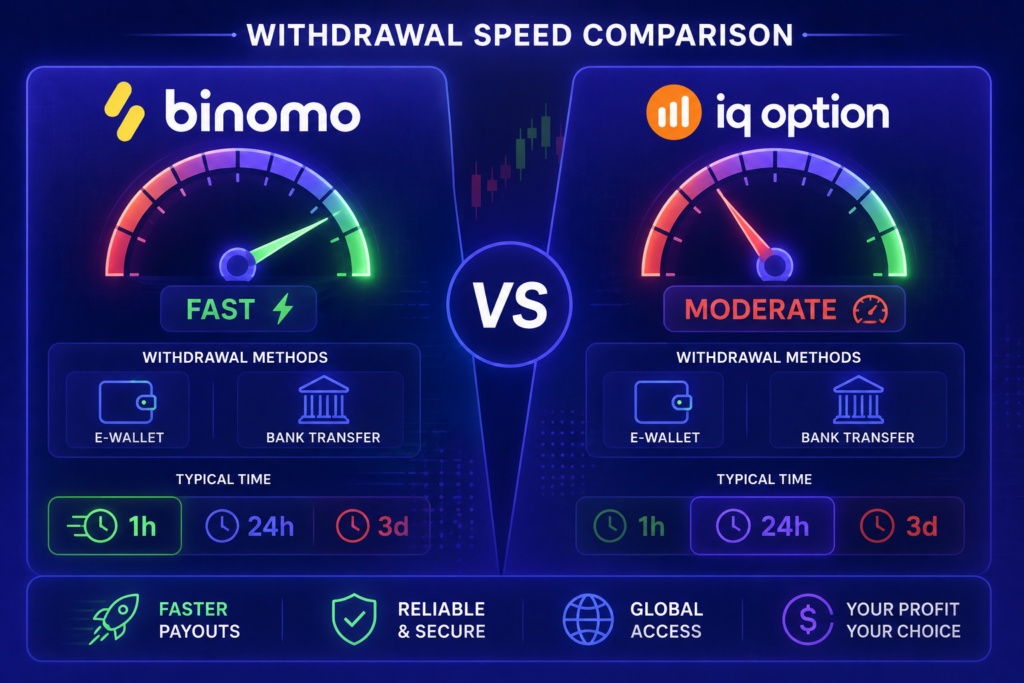

Binomo Withdrawal Speed Overview

Binomo is widely used by beginner traders because of its simplified interface and low deposit options.

Typical Withdrawal Time

Standard processing: 1 to 24 hours (after approval)

Some cases: up to 3 business days depending on method

Key Points

Binomo tends to process withdrawals faster when:

Account is fully verified

Same payment method is used for deposit and withdrawal

No bonus conditions are active

However, delays can happen if verification documents are incomplete or if bonus trading conditions are not met.

Strengths

Fast internal processing after approval

Multiple payment options including e-wallets and cards

Generally predictable withdrawal structure

Weak Points

Occasional delays during high-volume periods

Strict verification checks for larger withdrawals

IQ Option Withdrawal Speed Overview

IQ Option is known for a more regulated and structured withdrawal system, especially in regions where compliance requirements are strict.

Typical Withdrawal Time

E-wallets: 1 to 24 hours (often faster after first withdrawal)

Bank cards: 1 to 3 business days

Bank transfers: 3 to 5 business days

Key Points

IQ Option emphasizes security and compliance, which can slightly increase processing time but improves fund safety.

Strengths

Very stable payout system

Fast e-wallet withdrawals

Strong regulatory framework

Weak Points

Bank withdrawals can be slower

Verification steps may delay first withdrawal

Processing depends heavily on payment method

Binomo vs IQ Option Withdrawal Speed Comparison

Factor

Binomo

IQ Option

E-wallet speed

Fast (same day possible)

Very fast (often under 24h)

Card withdrawals

1–3 days

1–3 days

Bank transfer

2–3 days

3–5 days

First withdrawal

Moderate speed

Slightly slower due to KYC

Consistency

Stable

Very stable

Simple Insight

If you want quicker first-time simplicity, Binomo feels faster

If you want long-term stable payouts, IQ Option is more consistent

In real trading conditions, both platforms are competitive, but payment method choice matters more than the broker itself.

What Actually Affects Withdrawal Speed (Most Traders Miss This)

Many beginners think the broker controls everything. In reality, these factors matter more:

1. Verification Level

Unverified accounts always face delays. Full KYC speeds everything up.

2. Payment Method

E-wallets are consistently faster than cards or bank transfers.

3. Bonus Usage

If bonus conditions are active, withdrawals may be restricted until requirements are met.

4. Withdrawal Timing

Weekend and high-volume periods can slow processing.

5. Account History

New accounts often face longer first withdrawals for security checks.

Which One Is Better for Fast Withdrawals?

There is no absolute winner here.

Binomo is slightly more flexible for beginners who want quick access

IQ Option is more stable for long-term, regulated withdrawal consistency

But in both cases, your withdrawal speed depends more on:

Payment method

Verification status

Trading behavior

Suggested Internal Reading for Smarter Decisions

If you want to go deeper into broker selection and real performance testing, these guides will help:

Each design should follow a blue-purple trading UI theme, minimal text, and strong visual hierarchy for social media performance.

Smart Trading Insight (Most Important Part)

Fast withdrawals only matter if you are consistently profitable.

Many traders focus on payout speed but ignore:

Risk management

Entry timing

Emotional trading behavior

If your strategy is weak, even instant withdrawals won’t help long-term success.

You can improve execution and timing consistency with structured tools and analysis systems.

Final Step: Trade Smarter with BeCoin Premium

If you want a more structured approach with deeper market analysis, multiple timeframe insights, and trading system support, you can explore premium access here:

Which Is Easier for Beginners: Binomo or IQ Option?

For most beginners, the hardest part of trading is not strategy. It is surviving the first few months without blowing the account from emotional decisions, overtrading, and poor risk management.

That is why choosing the right platform matters more than many new traders realize.

Two names dominate beginner conversations in binary and short-term trading: Binomo and IQ Option. Both platforms attract new traders because of low deposits, simple interfaces, and fast market access. But they are not identical experiences.

Some beginners prefer Binomo because it feels simpler and less overwhelming. Others prefer IQ Option because it offers more tools, more chart flexibility, and a more professional trading environment.

So which one is actually easier for beginners in 2026?

The answer depends on what type of beginner you are.

Quick Verdict

If you want the shortest learning curve and the simplest interface possible, Binomo is usually easier to start with.

If you want more advanced charting, more trading tools, and room to grow long term, IQ Option may be the better choice.

The real question is not just which platform looks easier. It is which platform helps you avoid beginner mistakes while building consistency.

New traders often choose a platform based on hype, bonuses, or social media screenshots.

That is usually a mistake.

The best beginner platform is not the one with the biggest promises. It is the one that helps you make fewer emotional decisions.

Many beginners lose money because they jump into trades without structure. If you have not already seen it, read this breakdown of why 90% of traders lose money. Most losses come from behavior problems, not from lacking indicators.

A beginner-friendly platform should help you:

Learn slowly

Practice risk control

Avoid revenge trading

Focus on consistency

Use demo properly

Build a repeatable routine

This is where the differences between Binomo and IQ Option become important.

Binomo for Beginners

Binomo became popular because it removed complexity.

The interface is clean, lightweight, and extremely simple to understand even if you have never traded before. Many beginners can place trades within minutes of creating an account.

That simplicity is both an advantage and a danger.

What Makes Binomo Easier?

The platform feels less intimidating than many competitors. New traders are not overloaded with technical tools immediately. That lowers the friction to start practicing.

Key beginner advantages include:

Simple trading interface

Fast account setup

Easy demo switching

Low entry barrier

Minimal chart clutter

For someone completely new to trading, this creates a smoother first experience.

You can start with a demo account and focus on understanding candles, timing, and discipline before diving into complex indicators.

More tools create more confusion for inexperienced traders.

Many beginners open IQ Option and instantly overload charts with indicators they do not understand. That leads to analysis paralysis and emotional decision making.

This is why structure matters more than platform choice.

Skipping verification may sound convenient, but it can create withdrawal problems later if traders do not understand the risks.

Realistically, Which One Should You Choose?

Choose Binomo if:

You are completely new

You want maximum simplicity

You get overwhelmed easily

You mainly want to practice basic entries first

Choose IQ Option if:

You want deeper chart analysis

You plan to grow long term

You want stronger tools

You are serious about learning technical trading

Neither platform guarantees success.

The trader matters more than the broker.

A disciplined trader with a small account can outperform an emotional trader using the best platform in the world.

The Real Edge Beginners Need

Most beginners focus too much on entries and not enough on analysis quality.

Random signals and emotional trades usually fail because traders ignore higher timeframe structure.

That is where serious analysis changes everything.

At BeCoin Premium, traders get multi timeframe market analysis designed to help reduce emotional decisions and improve trade quality. Instead of guessing direction from one chart, you learn how higher timeframe momentum, structure, and confirmation work together.

If you want an extra edge instead of trading blindly, explore the BeCoin Premium plans.

Better analysis does not remove risk, but it can dramatically improve decision quality over time.

Final Thoughts

Binomo is easier at the beginning.

IQ Option is stronger long term.

The best choice depends on whether you value simplicity or growth potential more.

But regardless of platform, beginners who survive usually have three things in common:

They use proper risk management

They avoid emotional trading

They follow structured analysis instead of random entries

Your broker matters.

Your discipline matters even more.

Binomo vs IQ Option for Small Accounts: Which Platform Is Better for Beginners in 2026?

Most people entering online trading do not start with thousands of dollars.

They start small.

Usually with $10, $20, or maybe $50.

That small balance changes everything about how a trader behaves. Every loss feels bigger, every win feels emotional, and every mistake has a stronger impact on the account.

This is exactly why beginner traders constantly compare Binomo and IQ Option.

Both platforms are built around accessibility. They allow small deposits, offer fast onboarding, provide demo accounts, and simplify short term trading for beginners. On the surface, they look very similar.

But when real money becomes involved, important differences start to appear.

Some traders prefer Binomo because it feels simpler and less overwhelming. Others prefer IQ Option because of its stronger charting tools and more advanced analysis features.

The problem is that most comparison articles only scratch the surface.

They repeat generic statements without explaining how these platforms actually affect beginner psychology, risk management, and long term survival for small account traders.

This guide goes deeper.

We will compare Binomo vs IQ Option specifically from the perspective of traders using small balances and trying to grow consistently without blowing their account in the first week.

Why Small Account Traders Need a Different Type of Broker

Most online broker reviews are written for experienced traders.

That creates a huge disconnect.

A trader using a $10 account has completely different needs compared to someone trading with $5,000.

Small account traders care more about:

Simplicity

Emotional control

Fast execution

Low minimum deposits

Easy learning curve

Flexible risk management

Beginner friendly design

A complicated platform can actually hurt beginners.

Too many indicators, too many buttons, and too many market options often lead to impulsive trading behavior.

This is why platform structure matters far more than most people realize.

Before choosing any broker, you should understand the realities of low balance trading.

Binomo became popular mainly because of its simplicity.

The interface is clean, lightweight, and intentionally beginner focused. Unlike more advanced platforms, Binomo removes much of the complexity that overwhelms new traders.

For many beginners, that simplicity feels comfortable.

What Makes Binomo Attractive for Small Accounts

The biggest strength of Binomo is accessibility.

New traders can quickly understand how the platform works without spending weeks learning complicated trading software.

The platform is especially popular among traders who:

Use mobile devices

Prefer fast trades

Want minimal distractions

Trade with low balances

Need a simple learning environment

Binomo also tends to feel psychologically lighter for beginners.

Many traders underestimate how dangerous complexity can become when emotions are already high.

A simpler interface often reduces impulsive decisions.

Where Binomo Feels Limited

The simplicity becomes a weakness over time.

As traders improve, many begin wanting:

Better charting tools

More advanced indicators

Deeper market analysis

Stronger multi timeframe support

More technical flexibility

This is where some users begin feeling restricted.

Another issue is that traders sometimes become too dependent on fast trading behavior instead of learning proper market structure analysis.

That can create bad habits if risk management is weak.

IQ Option Overview for Small Traders

IQ Option takes a different approach.

Instead of extreme simplicity, the platform tries to combine beginner accessibility with more advanced trading tools.

This makes IQ Option feel more professional immediately.

Why Many Traders Prefer IQ Option

The biggest advantage of IQ Option is analytical flexibility.

Compared to Binomo, the charting environment is stronger and more suitable for technical traders.

Users gain access to:

More indicators

Better chart customization

Cleaner analytical workflow

More advanced tools

Stronger multi timeframe visibility

For traders serious about learning technical analysis, this becomes important over time.

IQ Option also tends to feel more scalable for long term development.

Instead of outgrowing the platform quickly, traders can gradually improve their analysis skills within the same environment.

The Hidden Problem With IQ Option

More tools do not automatically create better trading.

In fact, beginners often become more emotional when they suddenly gain access to advanced indicators and complicated chart setups.

This creates a dangerous illusion of control.

Many small account traders start adding:

Too many indicators

Random strategies

Emotional entries

Overtrading behavior

Unnecessary complexity

As a result, they lose faster despite having “better tools.”

This is why trading psychology matters more than platform features alone.

Binomo is usually better for traders who want simplicity and lower mental pressure during the learning phase.

IQ Option is generally better for traders who want stronger chart analysis tools and long term technical flexibility.

But neither platform automatically creates profitable traders.

That depends entirely on:

Risk management

Discipline

Market understanding

Emotional control

Trading structure

The platform is only the environment.

The strategy and psychology still decide the outcome.

Final Recommendation for Small Account Traders

If you are completely new and easily overwhelmed, Binomo may provide a smoother starting experience.

If you already understand basic charting and want deeper analysis tools, IQ Option usually offers more long term growth potential.

In both cases, avoid rushing.

The goal should not be turning $10 into a fortune overnight.

The goal should be surviving long enough to actually develop skill.

Start With the Right Platform

If you want a beginner friendly trading environment with a simple interface for small balance trading, you can explore Binomo here: Start Trading on Binomo

If you want stronger charting tools and a more advanced analytical environment, you can explore IQ Option here: Open an IQ Option Account

Want an Edge Beyond Random Trading?

Most traders lose because they enter trades without understanding the bigger market picture.

At BeCoin Premium, the focus is not random hype signals.

The goal is structured trading with real market context.

Inside BeCoin Premium you get:

Multi timeframe market analysis

High probability trade zones

In depth technical breakdowns

Smarter entry confirmation

Risk focused trading plans

Structured market direction updates

Instead of blindly taking trades, you learn how experienced traders analyze the market before entering positions.

$10 to $50 Trading Challenge – Strategy + Real Results (Case Study)

Turning $10 into $50 sounds easy until you actually try it. Small accounts expose every weakness in your trading. One bad decision can erase hours of progress, and emotional trading becomes much harder to control when every dollar matters.

This case study breaks down how a $10 account was realistically grown to $50 using a structured approach. No hype, no shortcuts, just a repeatable framework that focuses on control before profit.

The Real Goal Behind This Challenge

The goal was not fast money. It was controlled growth.

Most beginners fail because they rush. They overtrade, increase lot sizes too early, and ignore risk. This challenge flipped that approach by focusing first on protecting the account, then scaling gradually.

The strategy was intentionally simple to reduce errors. It focused on reading market structure instead of relying on complex indicators.

Trades were taken on a lower timeframe but always aligned with the higher timeframe trend. Support and resistance zones acted as decision points, and entries were only taken after confirmation, not prediction.

Instead of chasing trades, the focus stayed on control. Only a few trades were taken per session. Trading stopped after consecutive losses. Position size only increased after consistent growth.

Most traders skip this part and focus only on entries, which is why they struggle. If you want to understand the real reasons behind failure, read Why 90% of traders lose money

Day-by-Day Results Breakdown

The growth was steady, not aggressive.

Day 1 started with $10 and closed slightly above $12. The focus was testing execution and managing emotions. You can see the full breakdown here Real Day 1 $10 trading results

Over the next few days, the account grew gradually. The key shift was reducing unnecessary trades and waiting for cleaner setups. Confidence improved, but risk rules stayed unchanged.

By Day 4 and Day 5, small scaling was introduced. There was still no aggressive compounding, just controlled growth.

By Day 6 and Day 7, the account crossed $50. The important detail is that this was achieved without risking the account at any stage.

What Actually Worked

The biggest advantage was patience.

Fewer trades led to better decisions. Waiting for confirmation improved win rate. Emotional control made more impact than any indicator.

Most beginners fail because of predictable habits. Overtrading after a win, increasing size after a loss, and entering without confirmation are the most common ones.

If you want to avoid these completely, this breakdown explains them clearly Biggest beginner mistakes that kill trading accounts

Withdrawal and Platform Safety

Another critical part of this challenge was testing withdrawals.

Before scaling any account, it’s important to confirm that withdrawals actually work. Start small, verify your account, and use consistent payment methods.

This is not a shortcut to quick money. It is a discipline test. If you follow structure, it works. If you chase speed, it fails.

The Real Limitation Most Traders Face

Basic strategies can take you only so far. At some point, results become inconsistent because the market requires deeper understanding.

Most traders struggle here because they rely only on surface-level setups without context.

Final CTA – Build a Real Trading Edge

If you want to move beyond basic strategies and actually build consistency, structured guidance makes a difference.

Join BeCoin Premium and access advanced multi-timeframe analysis

Inside, you get deeper market insights, refined setups, and risk frameworks that help you trade with clarity instead of guesswork.

Final Thought

Turning $10 into $50 is not about finding a perfect strategy. It is about control, patience, and consistency.

If you can manage a small account properly, scaling becomes much easier later. Most traders fail not because they lack knowledge, but because they fail to follow a structured approach consistently.

I Started with $10 on Quotex – Day 1 Results (Real Case Study)

Most beginner traders ask the same question: Can you actually grow a small account like $10?

Instead of theory, I decided to test it in real conditions.

This is a Day 1 case study of trading with $10 on Quotex, documenting everything from setup to execution, mistakes, emotions, and actual results.

No hype, no fake screenshots, just a realistic breakdown of what happens when you start small.

Because choosing the right platform can make or break your first experience.

Simple Daily Trading Routine for Consistency

Most traders do not fail because of strategy alone. They fail because they are random. They trade when emotional, skip planning, increase risk after losses, and ignore review sessions. Consistency in trading usually comes from routine more than prediction.

A simple daily trading routine helps you stay disciplined, reduce emotional mistakes, and improve decision making over time. Whether you trade binary options, forex, or CFDs, structure matters.

This guide will show you a realistic daily routine that beginners can follow in less than one hour of preparation, plus how to choose platforms and tools that support steady progress.

Why Routine Matters More Than Strategy

Many traders spend months searching for the perfect indicator while ignoring habits. Even a good setup can fail when used without discipline.

Do not stare at charts all day. Trade during a defined session.

Examples:

London open

London and New York overlap

Evening OTC sessions if using binary platforms

Having a time window reduces boredom trades and random entries.

5. Journal Every Trade

After each trade, record:

Screenshot before entry

Why you entered

Risk size

Result

Emotional state

What could improve

Most traders skip this because it feels slow. That is exactly why they stay stuck.

6. End of Day Review (10 Minutes)

At the end of the day ask:

Did I follow my plan?

Did I overtrade?

Was my risk controlled?

Which setup worked best?

What mistake repeated today?

Review builds self awareness, which is often the missing edge.

Example Daily Routine for Busy Traders

A realistic schedule:

8:30 AM Check news and mark levels 8:45 AM Wait for session open 9:00 AM to 10:00 AM Trade only planned setups 10:05 AM Journal trades Evening Review screenshots and notes

Even one focused hour can outperform six random hours.

Best Platforms to Practice a Daily Routine

Execution speed, withdrawals, clean interface, and chart usability all matter. If you need platforms to test your routine, consider these options:

Quotex

Good for clean interface and beginner-friendly navigation. Open Quotex Account

A routine becomes stronger when backed by quality analysis. Many traders lose because they only watch one chart and one timeframe.

Professional traders often use:

Multi timeframe trend alignment

Session bias planning

Key liquidity zones

Entry confirmation timing

Risk mapped scenarios

Gain an Edge with BeCoin Premium

If you want a serious advantage, join BeCoin Premium for deeper market insight, multiple timeframe analysis, structured trading ideas, and smarter preparation before you trade.

When your routine meets quality analysis, consistency becomes much easier.

Final Thoughts

The traders who last longest are rarely the most aggressive. They are the most structured.

A simple daily trading routine can turn chaos into progress. Start small, protect capital, trade less, review more, and improve weekly.

Choose reliable platforms, follow risk rules, and if you want deeper guidance, use tools like BeCoin Premium to sharpen your edge consistently.

Manage Consent

We use cookies to store and access device data. Consent lets us process browsing behavior or unique IDs. Without it, some features may not work properly.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.