How I Mastered Correlation Trading in Binary Options

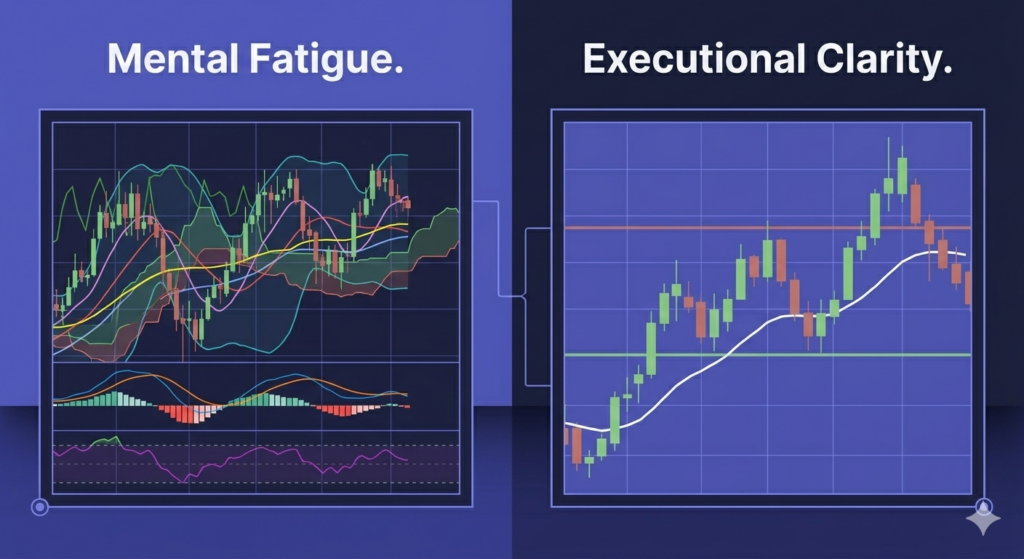

I still remember the night I almost threw my laptop across the room. I was staring at a 60-second EUR/USD chart, trying to predict whether the next candle would finish green or red. To me, it felt like flipping a coin in a dark room. I did everything the gurus told me to do. I loaded my screen with RSI, MACD, and Bollinger Bands until the actual price bars were barely visible. Still, my account balance kept bleeding.

That was the day I realized a harsh truth. I was looking at the market in absolute isolation. I treated the EUR/USD like it was the only financial instrument on the planet.

Everything changed when I accidentally opened two chart windows side by side: Gold and the AUD/USD currency pair. As Gold began to climb, a few minutes later, the AUD/USD followed it upward like an obedient shadow. They weren’t identical, but they were deeply connected.

That was my introduction to correlation trading. It is the strategy that took me from a frustrated novice to a trader who actually understands why the markets move. If you are tired of losing trades because a single candle suddenly spikes against you, let me share how looking at the bigger picture can completely transform your binary options journey.

The Epiphany of the Connected Market

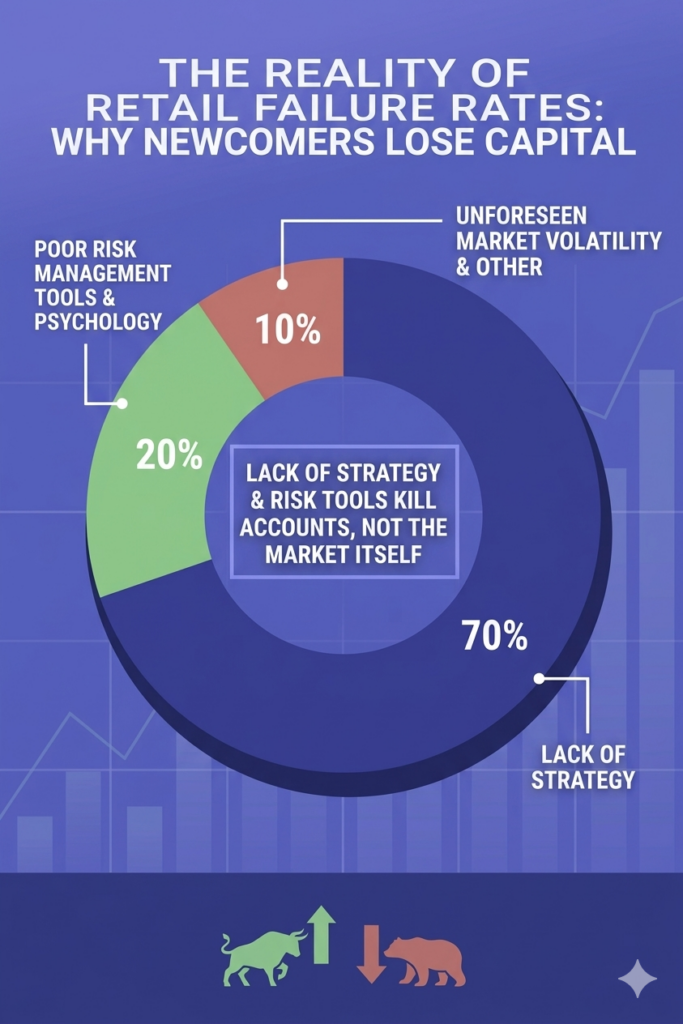

When you are starting out, binary options look deceptively simple. You choose an asset, select an expiry time, and click “Higher” or “Lower.” Because of this simplicity, it is incredibly easy to fall into bad habits. In fact, understanding how assets interact is one of the main differences between those who find consistency and the overwhelming number of people who fail. If you want to know more about those early traps, you can read about why 90 percent of traders lose money to see exactly what to avoid.

Correlation trading is the practice of analyzing two separate assets that share a historical relationship to predict the price movement of one of them. In the financial world, assets do not move in a vacuum. Economies are tied together by supply, demand, and global politics.

When you learn to spot these relationships, you gain a massive advantage. Instead of staring at one chart and guessing where it will go, you watch a leading asset to see what your target asset is likely to do next. It is like having a weather forecast for your trades.

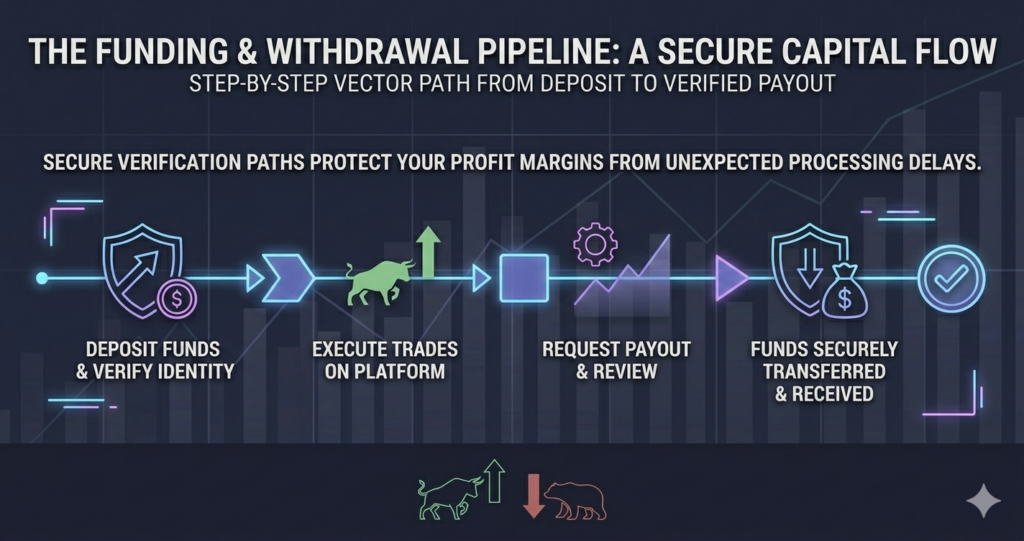

Before you can trade this strategy effectively, you need a platform that lets you view multiple charts simultaneously or switch between them instantly without lag. When I was testing this strategy, I spent a lot of time finding the right home for my funds. You can check out my breakdown of the top 3 trading platforms that actually pay to see which setups handle multiple asset analysis the best.

Positive and Negative Correlations Explained

To use this strategy, you need to understand the two ways assets interact: positive correlation and negative correlation.

Positive correlation means two assets move in the same direction. When Asset A goes up, Asset B goes up. A classic example is Gold and the Australian Dollar (AUD). Australia is one of the largest gold producers in the world. When the price of Gold rises, the Australian economy strengthens, which usually pushes the value of the AUD higher.

Negative correlation means two assets move in opposite directions. When Asset A goes up, Asset B goes down. The most famous example is the US Dollar (USD) and Gold. Because Gold is priced in US dollars globally, a stronger dollar makes Gold more expensive for overseas buyers, driving its price down. Therefore, if the USD index spikes upward, Gold typically drops.

When I first started executing these trades, I needed a broker with an interface clean enough to track these movements without giving me a headache. If you are struggling with a cluttered screen, take a look at my real comparison of which broker has the cleanest interface to make your charting experience much smoother.

My Go-To Correlation Pairs for Beginners

If you want to practice this strategy today on a demo account, here are the pairs I highly recommend monitoring:

Gold (XAU) and AUD/USD (Positive): Watch Gold for the leading move. If Gold breaks through a major resistance level and climbs, look for a “Higher” binary option opportunity on AUD/USD on the next candle.

Brent Crude Oil and USD/CAD (Negative): Canada is a massive exporter of oil. When oil prices rise, the Canadian Dollar strengthens. Because CAD is the second currency in the USD/CAD pair, a stronger CAD pushes the overall USD/CAD chart downward. So, when Oil goes up, look for a “Lower” option on USD/CAD.

EUR/USD and USD/CHF (Negative): The Euro and the Swiss Franc generally move together against the US Dollar. Because the USD is the base currency in USD/CHF and the quote currency in EUR/USD, these two pairs move like opposite mirrors. If EUR/USD rallies, USD/CHF almost always falls.

To trade these pairs smoothly, you need an environment with fast execution. I personally love comparing platforms to see which ones offer the best interface for tracking these pairs. For a direct comparison of two massive platforms, you can check out my guide on Deriv vs IQ Option for beginners in 2026 to see how they stack up for new traders.

How I Execute a Correlation Trade Step by Step

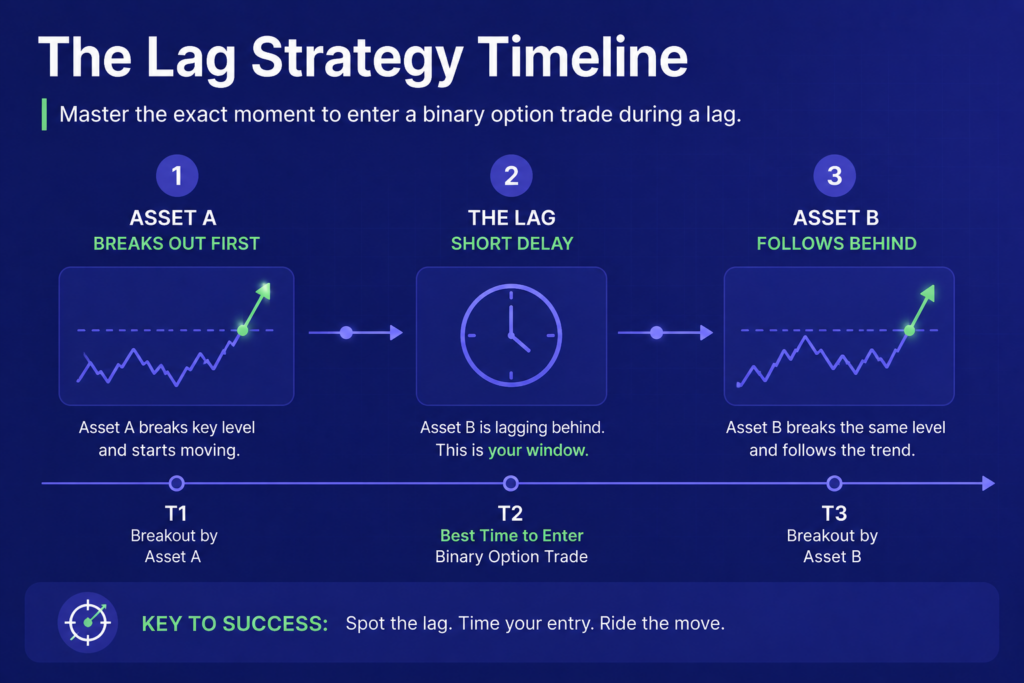

Let me walk you through exactly how I traded a negative correlation between the US Dollar and Gold just last week.

First, I opened two charts side by side. On the left was the US Dollar Index (DXY) or a major USD pair like USD/JPY. On the right was Gold (XAU/USD). I set both charts to the 5-minute timeframe.

Second, I waited for a market catalyst. I watched the USD/JPY break out of a morning consolidation zone, surging violently upward through a known resistance level.

Third, I looked over at my Gold chart. Because of the negative correlation, I expected Gold to drop. However, Gold hadn’t moved yet; it was stalling at the top of a recent bullish candle. This is what traders call a “lag.” The correlation gave me an early warning of what was coming.

Fourth, I quickly opened my binary options platform, selected Gold, set a 15-minute expiry time to give the market room to breathe, and placed a “Lower” trade. Within three minutes, the surging US Dollar dragged Gold down, and my trade cleared safely in the profit.

If you want to try this strategy on platforms that offer excellent charting tools, you can sign up and practice using the IQ Option registration portal or explore the multi-chart features available through the Binomo platform setup. Both platforms give you the visual flexibility needed to track these assets side by side.

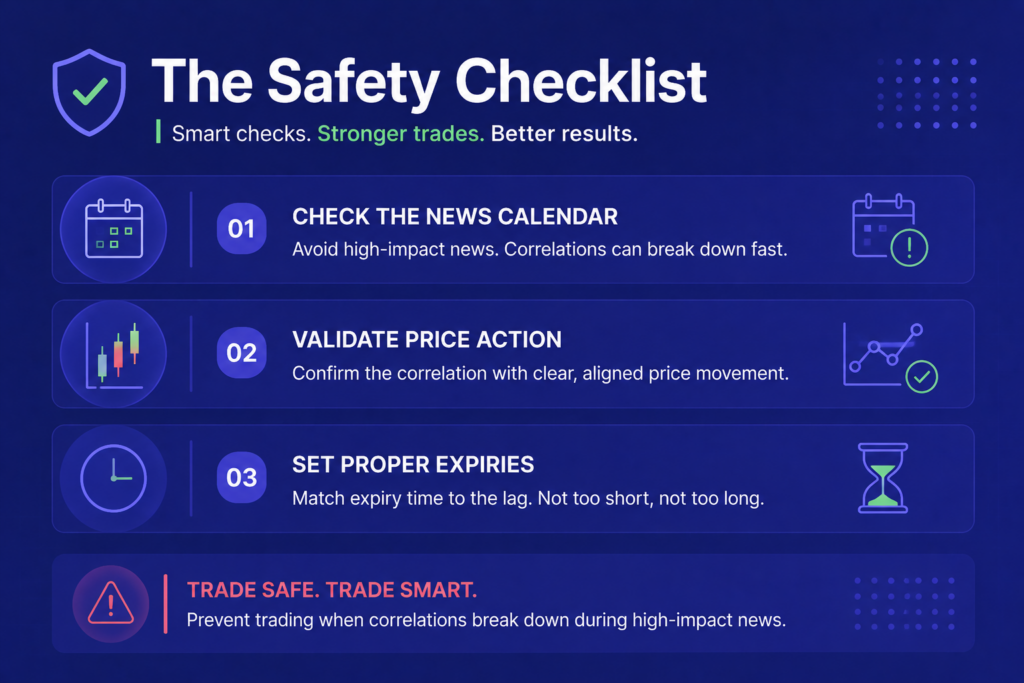

Managing the Risks of the Broken Correlation

Here is the warning the textbook writers won’t tell you: correlations do not work 100 percent of the time. They are tendencies, not absolute laws.

There are times when a correlation breaks down. For example, during a major global economic crisis, investors might rush into both the US Dollar and Gold at the exact same time looking for safety. Suddenly, a pair that usually moves in opposite directions is moving upward together. If you blindly place trades assuming the correlation holds, you will take losses.

To protect my capital, I never enter a trade based solely on correlation. I use correlation as an alert system. Once the correlation shows me a potential setup, I look at the target asset’s actual price action. If Gold should drop because the USD is rising, I wait until I see at least one bearish rejection candle on the Gold chart before clicking “Lower.”

Choosing the right broker also plays a huge role in risk management. You need a platform that offers transparent pricing and reliable expiries so your correlation analysis isn’t ruined by bad execution. For a deep dive into platform security, read my analysis on the safest trading platforms and their risk breakdowns to keep your capital secure.

Taking Your Technical Edge to the Next Level

Correlation trading completely changed how I look at financial markets. It took me away from the chaotic guessing games of short-term charts and forced me to think like a professional macro trader. Suddenly, the market made sense.

If you are just getting started and want to build your routine without risking massive amounts of capital, you can read my guide on how much money you really need to start trading for a realistic view of building an account. For those who want to jump right into practicing with other reliable brokers, you can also look into the Deriv tracking setup, try out the Pocket Option fast track, check out the Quotex registration gateway, explore ExpertOption accounts, or look at the tools provided on CapitalCore trading.

However, monitoring global macro relationships, tracking economic calendars, and calculating mathematical correlation coefficients by hand can become overwhelming if you are doing it completely alone. It takes hours of daily screening to find the highest-probability setups.

That is exactly why I stopped doing all the heavy lifting myself. If you want to skip the endless hours of chart watching and get straight to actionable data, you can view live market setups at the Becoin Forecast Hub.

If you are ready to truly gain a professional edge, stop guessing, and trade with deep analytical backing, unlock daily high-probability asset insights by joining the Becoin Premium Membership program today. Let the experts scan the correlations while you focus on executing flawless trades.

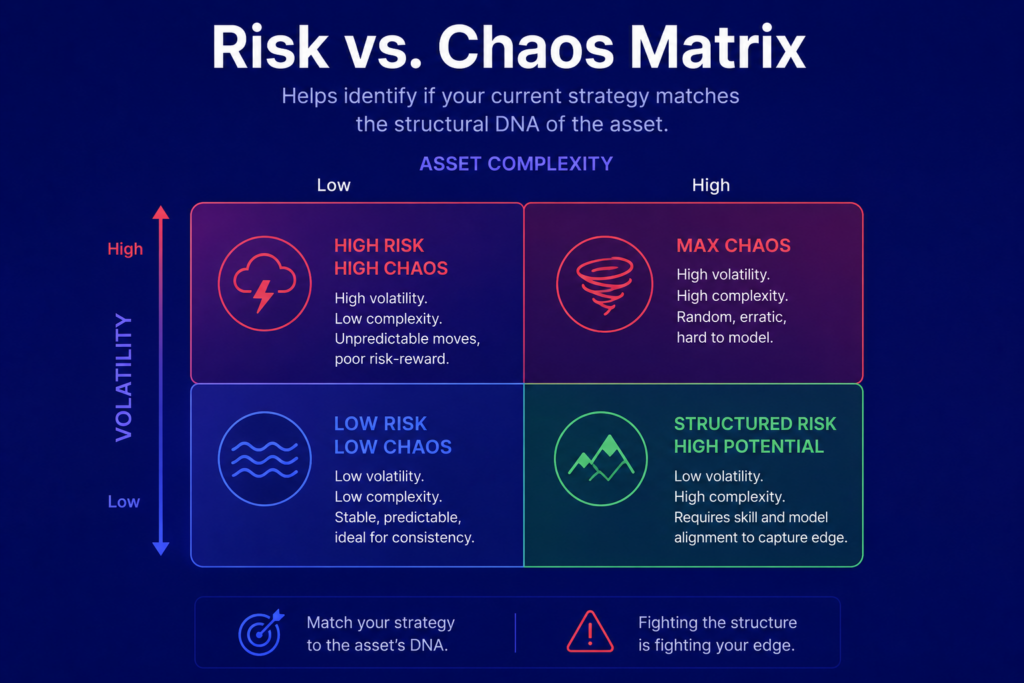

Why Some Assets Are Easier to Predict Than Others

I still remember the night I realized I was fighting a losing battle against a ghost. It was 2AM, my coffee had gone cold, and I was staring at a 1-minute chart of an exotic currency pair. Every technical indicator I threw at it failed. Support levels shattered like glass. Resistance lines vanished into thin air. I was applying textbook price action, yet the market was behaving like a toddler on a sugar rush.

The next morning, out of pure frustration, I switched over to a highly liquid asset during the peak of the London session. To my absolute shock, the candles moved with an almost poetic rhythm. They hit a level, paused, retested, and bounced exactly as the books predicted.

That was the day I stopped trading and finally started making money. It dawned on me that the problem wasn’t necessarily my strategy. The problem was that I expected every asset to play by the same rules. The truth is, some financial assets are hardwired to be more predictable than others. Understanding why this happens is the closest thing to a cheat code you will ever find in this game.

The Illusion of Uniform Markets

When you first step into the trading world, you are flooded with promises of universal strategies. The gurus tell you that if you master a head-and-shoulders pattern or a moving average crossover, you can apply it to anything from Bitcoin to soybeans and print money.

They are wrong.

Markets are not uniform entities. They are collections of human behavior, institutional algorithms, and structural rules. An asset’s predictability is determined by the invisible forces humming beneath the surface: liquidity, participant intent, and market structure. When I finally sat down to figure out how much money you really need to start trading, I realized that allocating capital to the wrong asset is the fastest way to turn a healthy account into a zero balance.

Let’s pull back the curtain on why some charts look like beautiful geometric steps, while others look like a heart monitor in an emergency room.

Liquidity and the Law of Large Numbers

To understand predictability, we have to talk about liquidity. Think of liquidity as a deep, massive ocean. If you throw a giant boulder into the Pacific Ocean, the water absorbs the impact, and the overall sea level barely moves. But if you throw that same boulder into a backyard swimming pool, you create a tidal wave that empties half the pool.

In trading, the boulder is an institutional order.

Major currency pairs like EUR/USD or heavily traded assets are the Pacific Ocean. Millions of traders, central banks, and algorithms are constantly buying and selling. Because there are so many participants, it takes an astronomical amount of capital to shift the price drastically. This creates a smoothing effect. Price action follows established trends because no single player can easily manipulate the market.

Conversely, when you trade illiquid assets or exotic pairs, you are trading in a swimming pool. A single hedge fund or an aggressive whale can step in, execute a relatively small order, and completely ruin your technical analysis. If you have ever wondered why 90 percent of traders lose money, it is often because they try to trade chaotic, illiquid environments where technical analysis breaks down completely.

For beginners trying to find their footing without drowning in noise, starting on platforms designed for clear execution is crucial. I spent months analyzing how different environments handle these structural shifts, documenting my observations in a breakdown of the safest trading platforms, which highlights how risk changes across various brokers.

The DNA of Predictable Assets

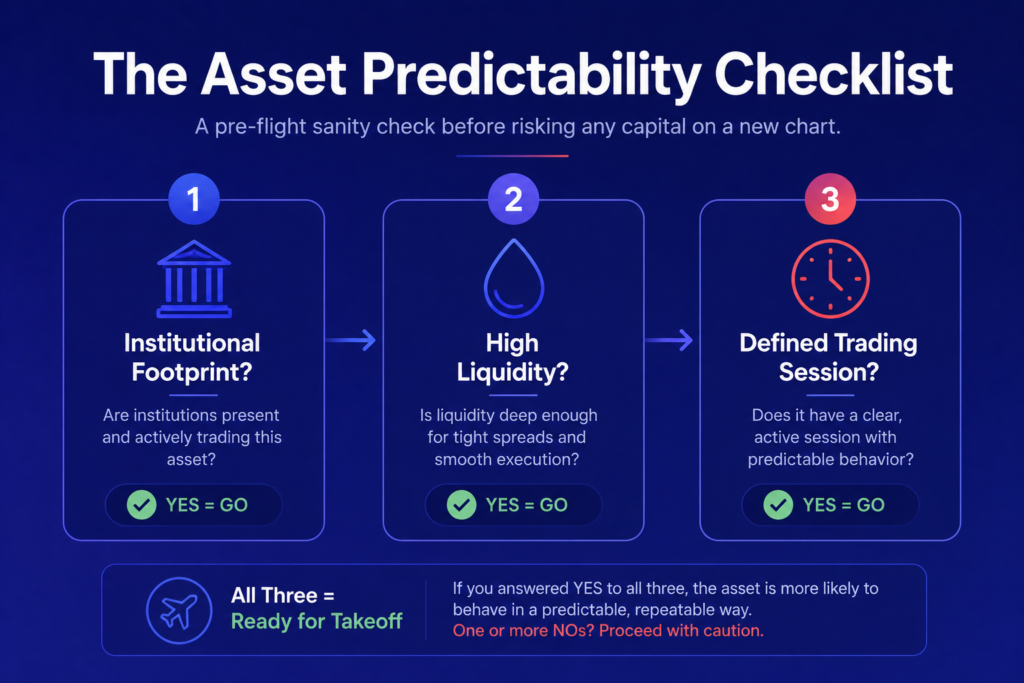

What makes an asset actually comply with your indicators? Through years of trial and error, I found that predictable assets share three core traits.

Clear Institutional Footprints

Institutions do not trade on gut feelings or 1-minute candle color changes. They buy and sell in zones, leaving massive footprints known as order blocks or support and recovery areas. Predictable assets have highly visible institutional interest. When the price retraces to a major daily level on a liquid asset, you can almost guarantee a reaction because major banks have automated buy orders waiting at those exact coordinates. Learning how to spot these zones completely changed my results when I was searching for the best broker for learning price action.

Session-Driven Rhythms

The most predictable assets adhere strictly to time. They possess a natural biological clock. If you track the major currency pairs, you will notice they come alive during specific hours and go completely flat during others. My entire perspective shifted when I stopped forcing trades at random times and leaned into the hidden rhythm of session-based trading. When a market has a defined open and close, volume pours in predictably, creating clean trends rather than choppy sideways traps.

Macroeconomic Alignment

A predictable asset moves based on visible fundamental realities, not just speculative hype. If the Federal Reserve raises interest rates, the US dollar strengthens. It is a logical, causal relationship. When an asset reacts logically to news, you can form a reliable hypothesis. When an asset moves purely based on social media tweets or speculative manipulation, predictability drops to zero.

The Wild West of Unpredictability

On the other end of the spectrum live the unpredictable assets. These are the charts that make you want to throw your laptop through a window.

Think about certain digital tokens, penny stocks, or exotic currency crosses. Why are they so volatile? It comes down to a lack of structural maturity. There are no massive central banks keeping the price stable. The order books are thin, meaning there is a massive gap between the buying price and the selling price.

In these environments, a chart pattern is practically useless. You might see a perfect bull flag forming, but because the market lacks depth, a single large market order can trigger a cascade of stop-losses, wiping out your position in milliseconds. I used to think I could tame these wild markets until I learned to sit on my hands during choppy conditions, accepting that survival matters more than being right in a chaotic environment.

Tailoring Your Strategy to the Asset

Once you accept that some assets are naturally easier to read, your job as a trader changes. You stop trying to force your favorite strategy onto an incompatible market. Instead, you hunt for the specific environment where your strategy has an unfair advantage.

If your strategy relies heavily on clean trends, Fibonacci retracements, and classic chart patterns, you belong in highly liquid, major macro markets. If you prefer rapid, short-term scalp trades based on pure volatility, you might look for faster-moving environments.

Finding this alignment is a deeply personal journey. I remember documenting my own struggles trying to find the right balance, which I wrote about in a personal account of chasing safety in a high-stakes world, where I detail how finding the right platform and asset class salvaged my career.

To help visualize how these factors stack up against each other, here is a quick breakdown of how predictability scales across different asset characteristics:

Asset Characteristic

Predictability Level

Primary Driving Force

Recommended Strategy

High Liquidity / Major Volume

High

Institutional Order Flow

Trend following, Price Action

Low Liquidity / Exotic Crosses

Low

Retail Speculation / Whales

Breakout trading with tight stops

Clear Session-Based Hours

High

Global Corporate & Bank Activity

Session-open momentum trading

Continuous 24/7 Speculative

Medium-Low

News Sentiment & Hype

Mean reversion, Risk-off scalping

For those just beginning to navigate these waters, selecting the right gateway is half the battle. If you want to see how the major entry-level choices stack up in real-world scenarios, check out my hands-on comparison between Binomo and IQ Option to see which one fits your daily operational routine best.

Navigating the Broker Landscape

Choosing what to trade is only part of the equation; where you trade it matters just as much. Different brokers cater to different styles of asset predictability.

For instance, if you are looking for an intuitive, smooth interface to practice reading clean asset movements, the IQ Option Registration provides an incredibly responsive charting engine that makes spotting price action fluid. On the flip side, if you value alternative market structures like synthetic indices, which emulate pure market mechanics without unexpected fundamental disruptions, checking out the Deriv Platform can offer an entirely different edge.

If you are exploring alternative brokers with highly competitive environments, you can look into the Pocket Option Sign-up or check the streamlined trading features available via the Quotex Portal. For those who prioritize rapid execution speeds during fast-moving news events, options like the ExpertOption Registration, the classic interface at Olymp Trade, or the institutional feel of Capital Core provide diverse environments to test your theories on asset predictability.

Moving Beyond Guesswork

At the end of the day, trading shouldn’t feel like a trip to Las Vegas. If you feel like you are guessing, you are likely trading an asset that lacks the structural integrity required for predictability. By aligning your strategy with highly liquid, session-driven assets, you remove a massive layer of randomness from your trading business.

But even with the best assets, navigating the markets alone can be an uphill battle. The real shifts happen when you stop guessing and start utilizing deep, institutional-grade analysis.

If you want to stop reacting to the market and start anticipating it with precision data, join the elite inner circle at the Becoin Tariff Plan and gain instant access to institutional-grade insights. For real-time updates and professional market direction breakdowns, bookmark the Becoin Forecast Hub to secure your unfair edge in the markets today.

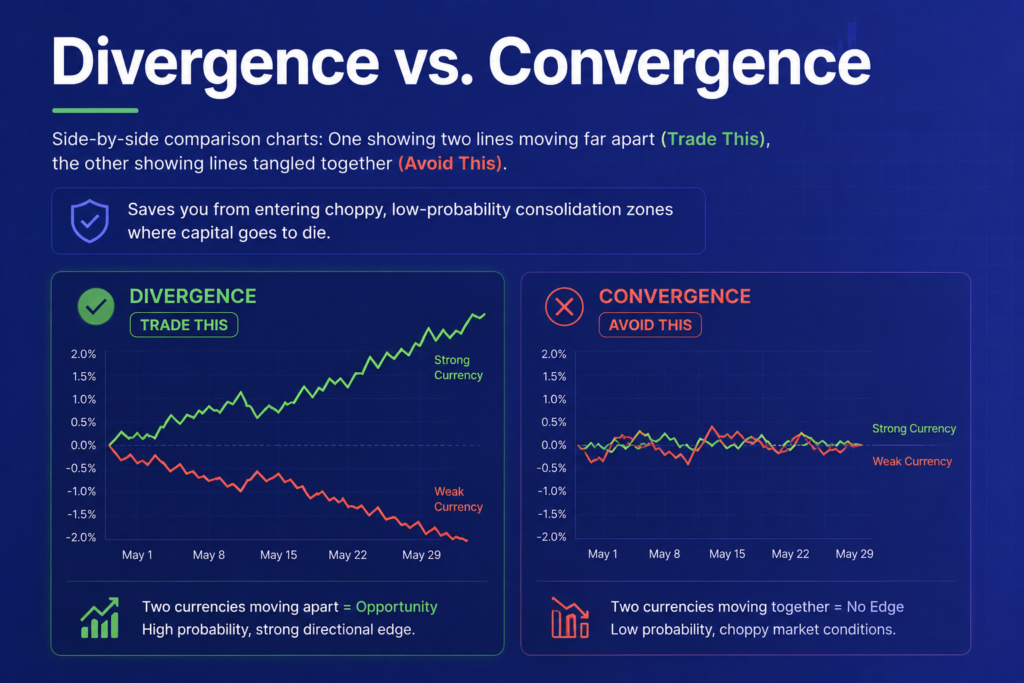

Trading Currency Strength Instead of Single Pairs

It was a Tuesday afternoon when I realized I was fighting a losing battle against a ghost. My screen was a chaotic web of indicators. I had the EUR/USD chart open, a moving average crossing over here, a relative strength index flashing oversold there, and a price action setup that looked textbook perfect. I clicked “Buy.”

Within four minutes, the trade tanked. Price slashed straight through my support level like it wasn’t even there.

Frustrated, I opened the GBP/USD chart to find a different setup. Shockingly, it was plunging too. I flipped over to AUD/USD. Same story. Red candles everywhere. I felt that familiar, sinking feeling in my chest. If you have ever wondered why 90% of traders lose money, look no further than this exact moment. I thought I was analyzing three independent charts, but I was actually just making the same blind bet against the US Dollar three times over.

I was looking at the individual trees and completely missing the forest fire. That was the day I stopped trading isolated pairs and started trading currency strength.

The Flaw of the Single Pair Lens

When most of us start out, we pick a pair like EUR/USD or GBP/USD because someone online said it has the highest liquidity. We treat that pair like a single stock. We study its support levels, its moving averages, and its quirks.

But a currency pair is not a stock. It is a tug-of-war between two entirely separate economies.

When you look at EUR/USD and see price going down, your brain naturally thinks, The Euro is weakening. But is it? What if the Euro is actually incredibly strong today, gaining ground against the British Pound, the Japanese Yen, and the Australian Dollar, but the US Dollar just happens to be experiencing a massive, unexpected surge due to an unannounced institutional inflow?

If you only look at EUR/USD, you are blind to that reality. You might take a short position on the Euro, only to watch it aggressively reverse because the Euro itself wasn’t weak at all. You were simply trading the wrong side of a hidden macro trend.

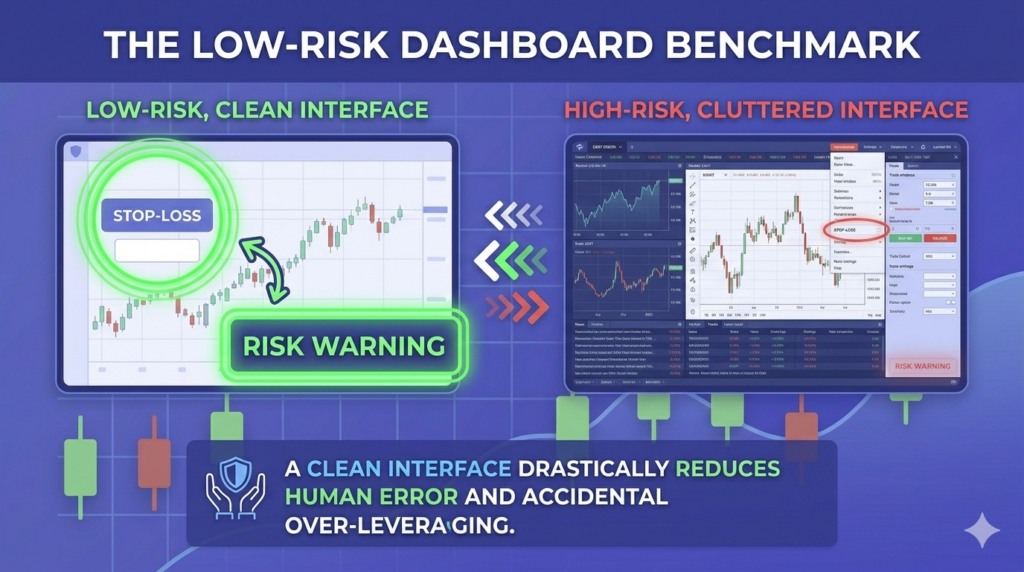

To fix this, I had to completely reshape how I viewed the market dashboard. I needed an environment that allowed me to see the raw velocity of individual currencies, not just their blended combinations. If you are still hunting for a workspace that gives you this kind of raw clarity without overwhelming your screen, check out this breakdown of which broker has the cleanest interface. Seeing the data clearly is half the battle.

Discovering the Currency Strength Matrix

The turning point for me came when I threw out my standard indicator stack and replaced it with a simple Currency Strength Matrix. This isn’t a complex, proprietary mathematical formula. It is an overlay that measures how an individual currency is performing against a basket of its peers over a specific timeframe.

Imagine eight runners in a race. If you only look at Runner A and Runner B, you can tell who is winning between the two, but you have no idea if they are both moving at a snail’s pace while the other six runners fly past them. A strength matrix lets you look down from the stadium press box and instantly see who is sprinting, who is jogging, and who is completely out of gas.

When I look at the market now, I look for extreme divergence. I want to pair the absolute strongest currency of the day with the absolute weakest currency of the day.

If the US Dollar is a rocket ship and the Japanese Yen is an anchor, I do not want to guess at support levels on EUR/USD. I want to trade USD/JPY. That is where the real, unadulterated momentum lives. This structural shift is what keeps you alive in volatile environments. It is a core philosophy I adopted while reading about how understanding market structure saved my binary options trading.

From Theory to the Live Terminal

Let me walk you through how this actually plays out when you sit down at your terminal. I start my session by opening a multi-currency heat map. I am not looking at candlestick formations yet. I am looking at percentages and directional velocity across the majors: USD, EUR, GBP, JPY, AUD, CAD, and CHF.

On a particular morning, the Euro was showing a clean +0.85% average gain across all its pairs. It was beating the Dollar, crushing the Pound, and stepping all over the Aussie. At the exact same time, the Canadian Dollar (CAD) was sitting at -1.10%, bleeding value across the board due to an overnight drop in crude oil prices.

The trade setup was screaming at me: EUR/CAD Long.

Instead of fighting the choppy, indecisive ranges of EUR/USD, I stepped into a market where the buyers were highly aggressive and the sellers were completely checked out. I opened my execution platform, verified the clean price action structure on the EUR/CAD chart, and executed the trade. Because I paired true strength with true weakness, the price didn’t linger or tease my stop loss. It moved cleanly, smoothly, and predictably into profit.

If you want to test this strategy yourself without risking a massive amount of capital, you can start small. I highly recommend checking out the entry barriers outlined in how much money do you really need to start trading. You don’t need thousands of dollars to practice reading true market velocity.

For execution on these momentum setups, I rely on platforms that offer fast order filling and zero lag, because catching a strength divergence requires precision. You can explore the live execution environments on IQ Option or set up a clean charting layout on Binomo to keep tabs on multiple asset classes simultaneously.

Filtering the Noise and Staying Cash

The greatest benefit of trading currency strength isn’t just that it shows you what to trade. Its real power lies in showing you what not to trade.

There are days when the strength matrix looks like a tangled ball of yarn. The USD is up a fraction, the EUR is down a fraction, the GBP is flat, and everything is hovering around the zero line. In the past, I would have forced a trade anyway. I would have zoomed down to the one-minute chart on GBP/USD, convinced myself I saw a double bottom, and given my money right back to the market.

Now, when the matrix shows convergence—meaning all currencies are performing relatively similarly—I sit on my hands. No divergence means no true trend. No true trend means no mathematical edge. If you struggle with the urge to trade during these dead zones, take a moment to read about my personal journey of learning how to sit on my hands during choppy markets. It will completely reframe how you view patience.

When the market context is right, you want an environment that won’t lock up your funds when it is time to harvest your wins. I always cross-reference my execution venues based on processing performance, which you can see in this independent test of the fastest withdrawal brokers.

For high-volume days where I want straightforward, lightning-fast contract entries without wading through bloated features, I use alternative matching engines like Pocket Option or Quotex. If you are caught between choosing platforms for your daily execution routine, you can read this direct breakdown on which is easier for beginners: Binomo or IQ Option to map out your specific infrastructure needs.

Elevate Your Analytical Horizon

Switching to currency strength took me out of the reactive, emotional loop of chasing individual candles and elevated me into a structural strategist. I stopped guessing where the market was going because I could finally see exactly where the capital was flowing in real time.

But a matrix tool is only your foundation. To truly scale your consistency and stay ahead of institutional shifts, central bank interventions, and hidden sentiment reversals, you need to go deeper than basic retail tools. You need institutional-grade forecasting, daily directional bias breakdowns, and real-time structural analysis.

This level of depth is exactly what we build inside our private network every single day. If you are tired of trading blind and want a definitive edge in your market analysis, explore our real-time data feeds at the Becoin Forecast Hub, and unlock our complete institutional toolkit by joining the Becoin Premium Tariff Plan. Let’s stop guessing at single pairs and start trading the actual flow of global capital together.

How Liquidity Affects Binary Options Results

When I first started trading binary options, I believed success was all about finding the perfect indicator. I spent weeks testing moving averages, RSI settings, support and resistance levels, and dozens of YouTube strategies that promised easy wins. Some worked for a few trades, but most failed.

What confused me was that the same setup could produce completely different results on different days. One morning, a simple breakout would run perfectly to expiry. The next day, the exact same setup would stall, reverse, and finish out of the money.

At first, I blamed the broker. Then I blamed the strategy. Eventually, I discovered the real culprit: liquidity.

Understanding liquidity completely changed how I approached binary options trading. More importantly, it helped me stop taking low-probability trades that looked attractive on the chart but had almost no chance of producing consistent results. If you trade binary options and have ever wondered why some days feel easy while others feel impossible, liquidity may be the missing piece.

What Is Liquidity in Trading?

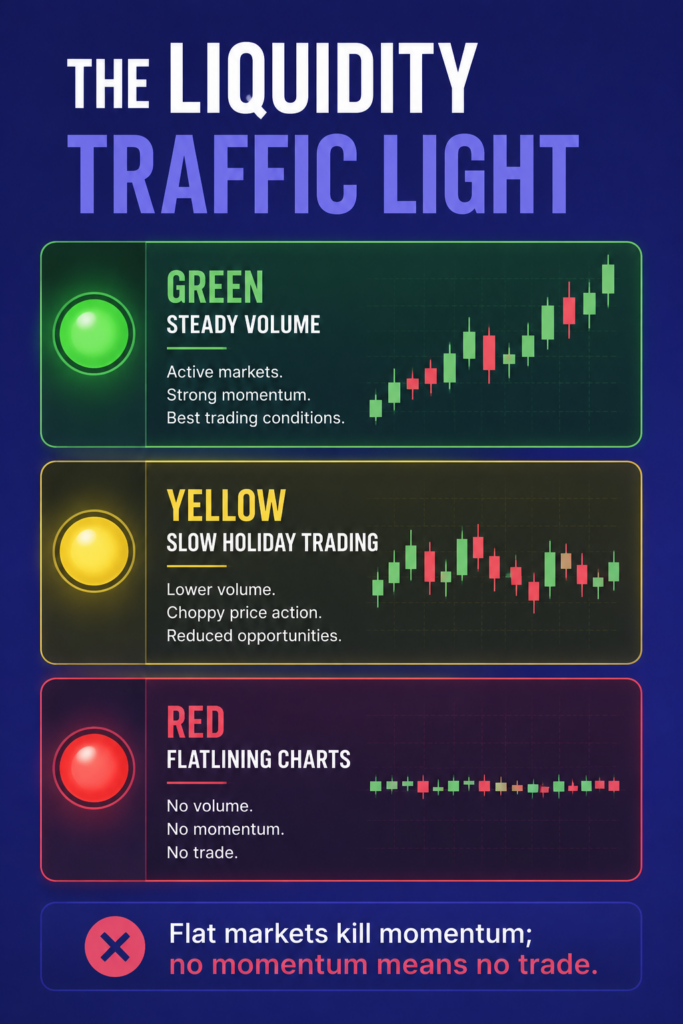

Liquidity refers to the amount of buying and selling activity taking place in a market.

High Liquidity: There are plenty of buyers and sellers participating actively.

Low Liquidity: Fewer market participants are active.

For binary options traders, liquidity matters because it directly affects how price moves. High liquidity creates cleaner price action, while low liquidity often creates random, erratic movements that are incredibly difficult to predict.

I learned this lesson the hard way. One evening, I found what looked like a perfect support bounce setup on EUR/USD. Everything aligned. The level had held multiple times, momentum indicators agreed, and the market structure looked healthy.

I entered confidently, but price suddenly spiked right through support for a few seconds before returning to the original direction. The trade expired as a loss. The next day I checked the chart and realized I had traded during a period of extremely low market activity. The setup wasn’t bad; the timing was. If you want to avoid these traps, finding your rhythm starts with choosing the right platform workspace, a journey I wrote about in Finding My Perfect Workspace: The Search for the Best Broker for My Daily Trading Routine.

Binary options depend entirely on one specific thing: where price closes at the exact expiry moment. Unlike traditional trading where you can hold positions longer to weather random spikes, binary traders need accurate, short-term price movement. That makes liquidity even more important.

When liquidity is strong:

Trends move more smoothly.

Support and resistance levels react more reliably.

Breakouts have greater follow-through.

Candlestick patterns become more meaningful.

Random market noise decreases.

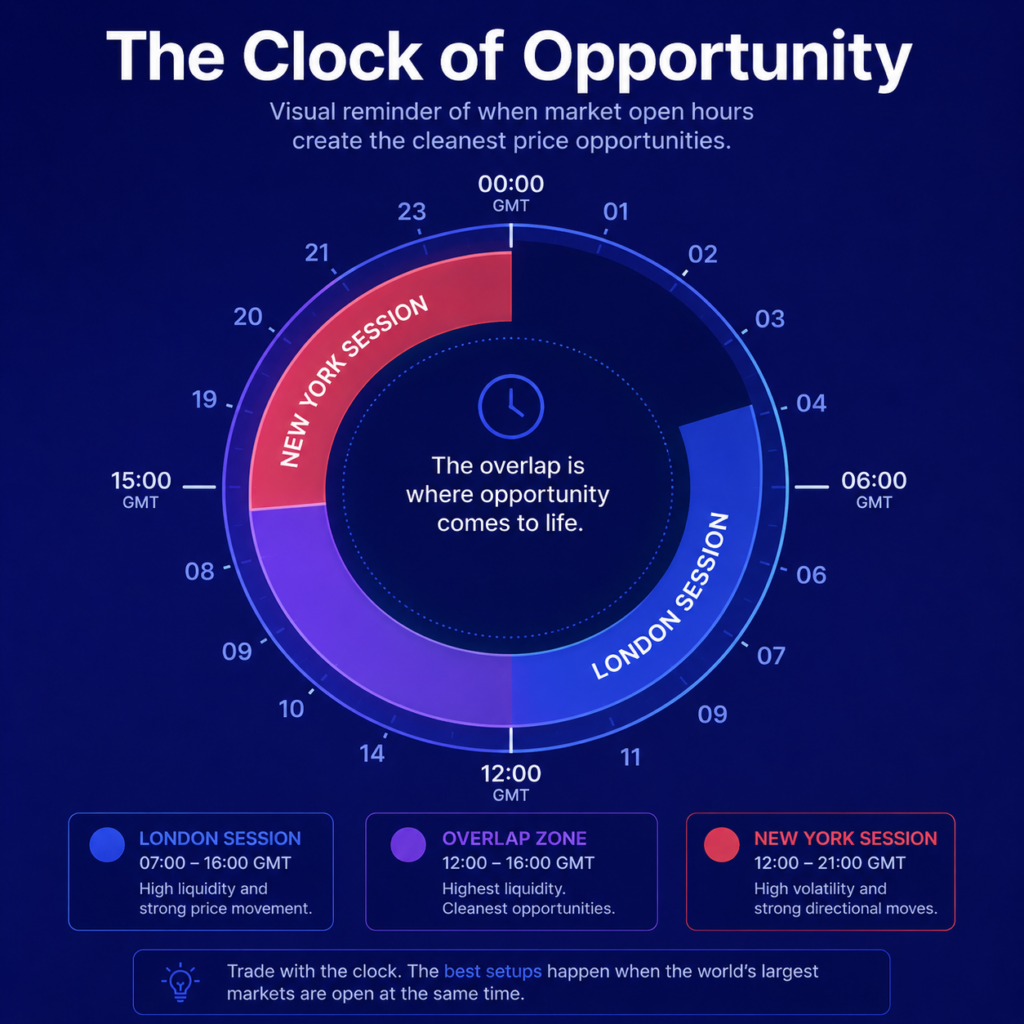

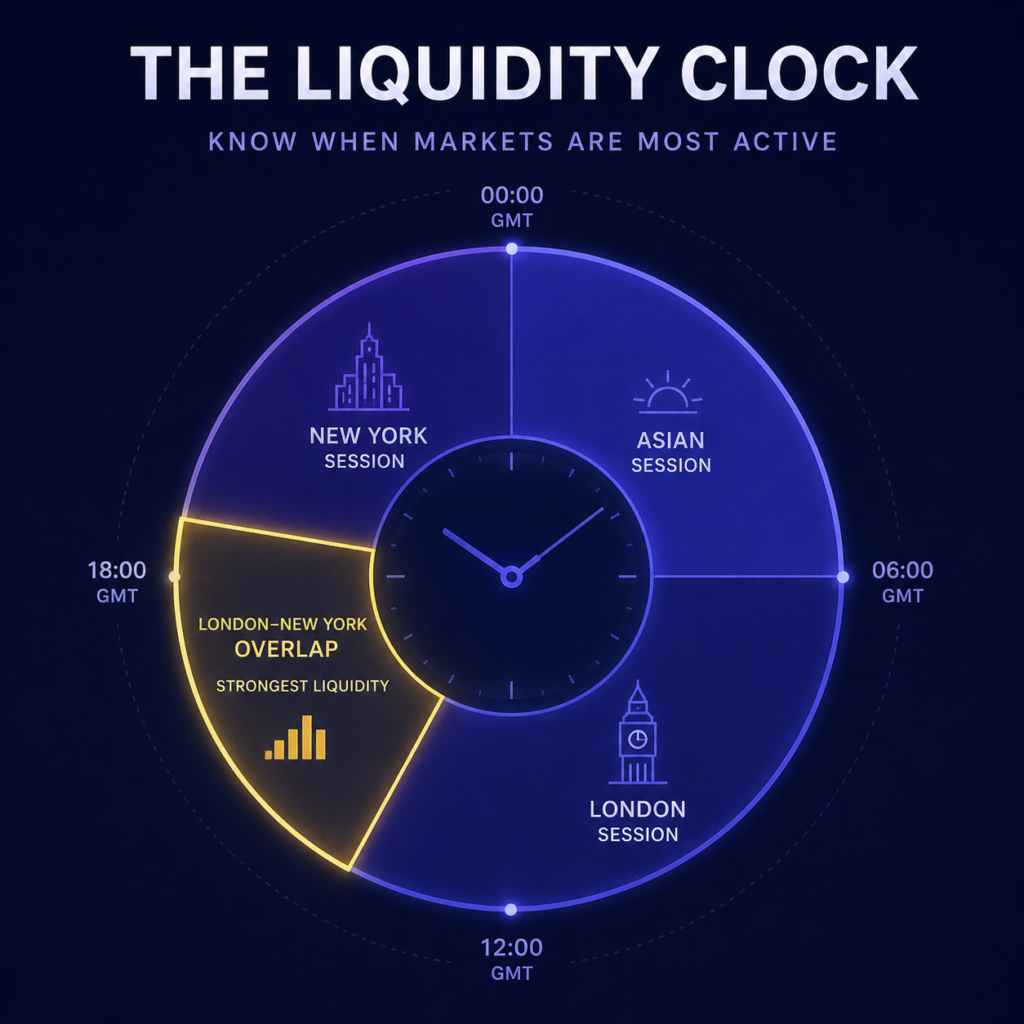

This is one reason session timing plays such an important role. In my experience, the best setups often appear when major financial centers overlap. The London and New York overlap remains one of the most active trading periods globally, where price moves with clear purpose rather than hesitation. If you want to understand how trading sessions influence your setups, read my detailed guide on The Clock and the Cash: My Journey Into the Hidden Rhythm of Session-Based Trading.

The Hidden Danger of Low Liquidity

Most beginners focus entirely on finding trades, whereas professionals focus on avoiding bad conditions. Low liquidity creates environments where probability becomes harder to measure. During these quiet times, you will often notice:

Long, unpredictable candlestick wicks

Sudden, unexplained reversals

Frequent false breakouts

Slow, grinding price movement

Choppy consolidations

I used to force trades during quiet periods because I felt I needed action. That mindset cost me more money than any structural strategy mistake. Eventually, I realized that choosing not to trade is often the best trading decision you can make.

One of the biggest breakthroughs in my trading came from tracking liquidity throughout the day. I noticed that the exact same strategy produced dramatically different results depending on the active trading session.

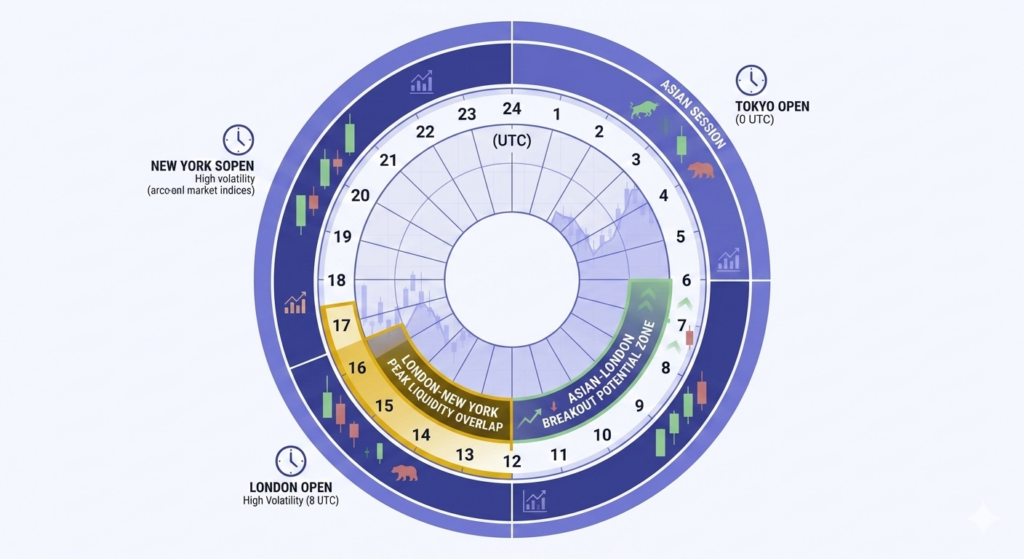

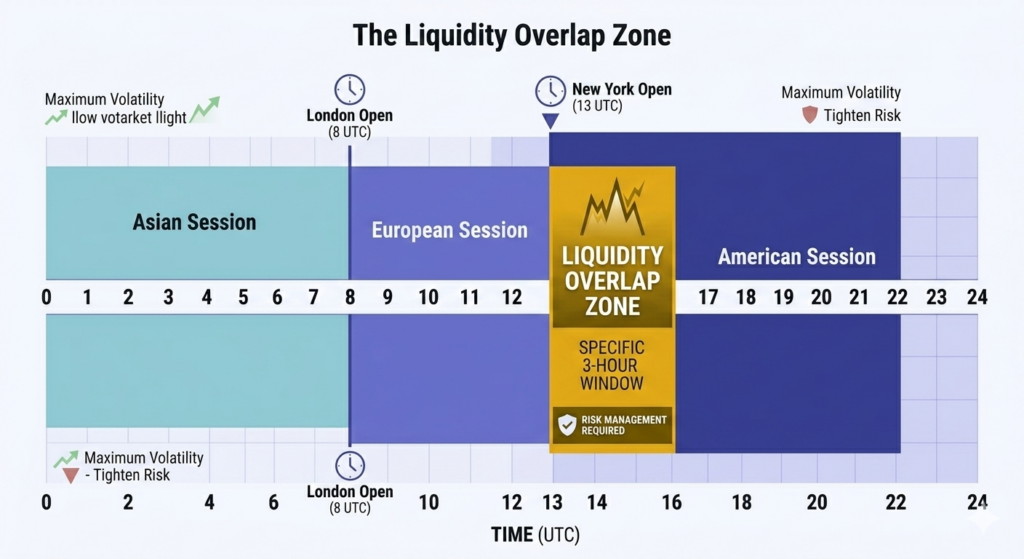

The strongest liquidity generally appears during:

The London Session: European markets generate substantial volume and often establish the core direction for the day. This environment makes it the best broker for learning price action in 2026 tested by real traders a crucial asset if you are trying to master structural movements.

The New York Session: American traders enter the market, creating heavy participation and clean momentum.

The London-New York Overlap: This is where the highest liquidity peak appears, and many of my best binary options trades occurred during this specific window.

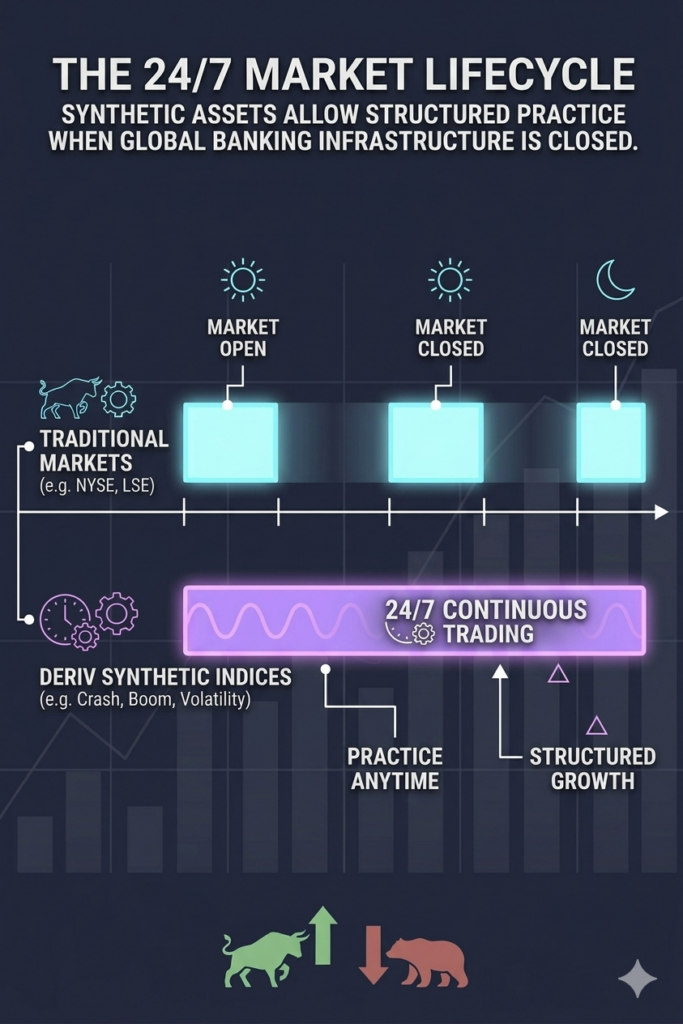

Meanwhile, low-liquidity periods often include late New York hours, holiday periods, and session transition dead zones. If you are restricted to trading outside these hours, you have to adjust your strategy completely. For instance, some platforms offer synthetic indices that mimic true market liquidity even on weekends. You can see how platforms handle this in our comparison of Deriv vs IQ Option for Synthetic Indices: Which Platform Is Better in 2026, or check out our guide on Why Market Open Hours Create the Best Trading Opportunities.

How Liquidity Impacts Common Binary Options Strategies

Liquidity affects nearly every strategy you deploy on your charts.

The Connection Between Liquidity and Trader Psychology

What surprised me most wasn’t the market impact; it was the intense psychological impact. Low-liquidity environments actively encourage overtrading. Because nothing seems to happen, traders become impatient. They start inventing setups, forcing entries, and abandoning their core discipline.

Ironically, the periods with the fewest real opportunities often generate the biggest account damage. This destructive behavioral loop is why so many beginners struggle to protect their balances. If you are wondering why consistency feels so elusive, our extensive breakdown in Why 90% of Traders Lose Money: Real Reasons Beginners Don’t Realize explores many of these hidden behavioral traps.

Choosing a Platform That Supports Better Trading Conditions

Liquidity itself comes from the broader global market, not individual brokers. However, platform quality still matters tremendously. Execution speed, chart responsiveness, available asset variety, and session accessibility all directly influence your ability to capitalize on liquid windows.

Many traders compare major platforms before choosing where to start out. If you are assessing your options, it helps to read real, head-to-head performance evaluations:

Today, before entering any binary options position, I force myself to answer five simple questions:

Is the underlying market currently active?

Am I trading during a major regional session or overlap?

Is the price moving cleanly without erratic, hyper-extended wicks?

Are technical support and resistance levels actively respecting historical structure?

Would I still take this exact setup if my trade volume size were twice as high?

If I cannot confidently answer “yes” to those questions, I walk away from the chart. The difference in my long-term account survival has been night and day.

Final Thoughts

For years I searched for a magic technical indicator, but the truth was much simpler. Market conditions matter far more than the tools you overlay on top of them. Liquidity influences trend quality, breakout reliability, support and resistance reactions, and overall predictability. Many losses that retail traders blame on strategy failure are actually liquidity problems in disguise.

Once I stopped chasing trades during quiet markets and focused heavily on high-participation periods, my daily results stabilized. If you’re serious about improving your binary options performance, start paying attention not only to where price is moving, but also to how much volume exists behind that move.

If you want deeper market analysis before placing your next trade, explore our Forecast Hub for comprehensive insights and daily market preparation. For traders who want a genuine structural edge, you can access institutional-style analysis, volume liquidity mapping, session planning, and premium asset forecasts through BECOIN Premium.

The biggest improvement in my career did not come from finding more trades. It came from learning which market environments were actually worth risking capital in the first place.

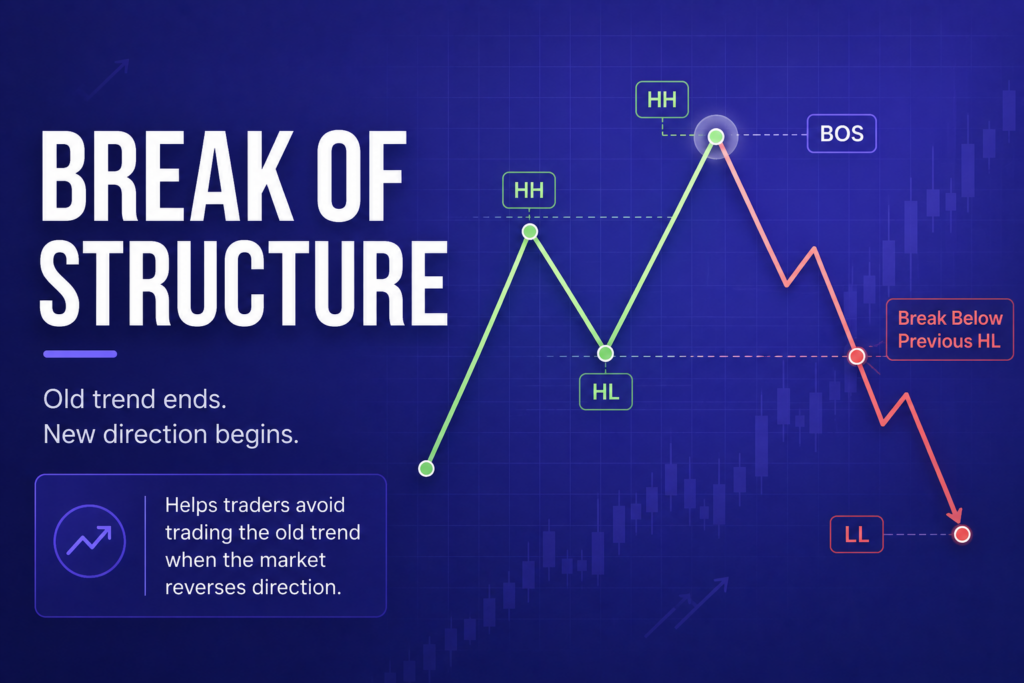

How Understanding Market Structure Saved My Binary Options Trading

I remember the exact moment my trading account hit zero for the third time in a single month. It was a rainy Tuesday evening, and I was staring at a 1-minute chart on my laptop screen. The price had been moving up aggressively. It looked like a flawless rocket ship to the moon. I clicked the green “Higher” button, confident that the momentum would carry my trade to an easy payout in sixty seconds.

Instead, the very next candle reversed with terrifying speed. It didn’t just drop; it crashed straight through my entry point, leaving me empty-handed. Desperate to recover the loss, I immediately entered a “Lower” trade, assuming the market was crashing. The market instantly flipped back upward.

I felt like an invisible entity was watching my screen, actively trading against me. If you have ever felt this way, you are not alone. It is exactly why 90% of traders lose money. We enter the market chasing colors and momentum without understanding the underlying architectural layout of the asset.

Everything changed for me when I stopped downloading messy technical indicators and started learning market structure. I realized that the market isn’t a chaotic ocean of random ticks. It is a highly organized, repetitive system driven by institutional order flow and retail psychology. Once you learn to read the architectural bones of a chart, binary options stop looking like a gamble and start looking like a game of calculated probabilities.

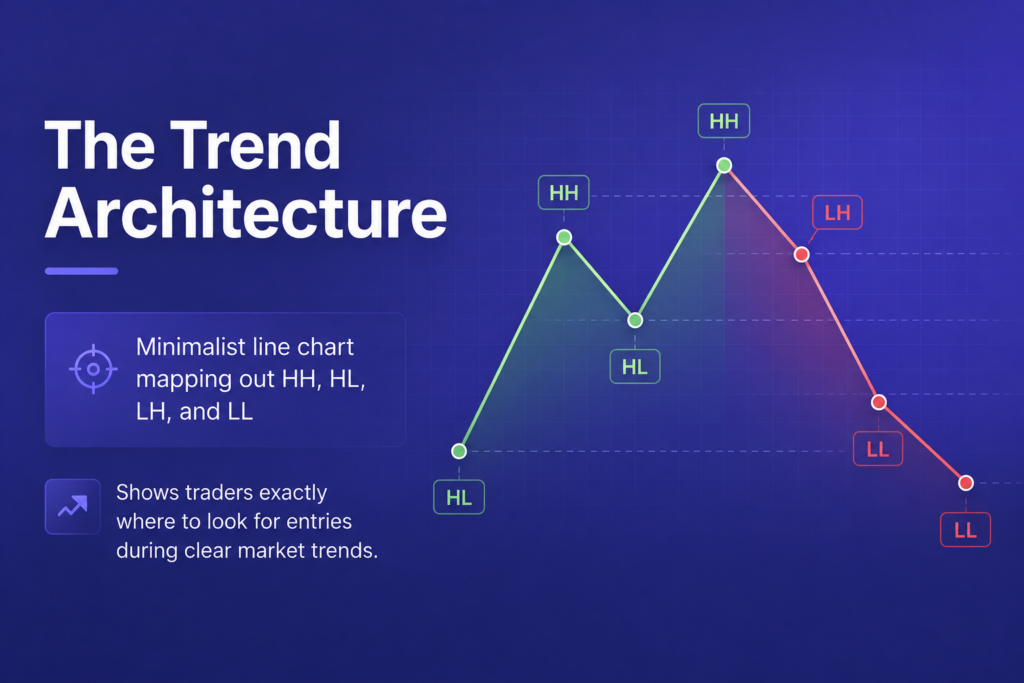

What is Market Structure and Why Does It Matter for Binary Options?

In simple terms, market structure is the study of the trend, the asset’s current phase, and the structural high and low points on a price chart. While forex or crypto traders use market structure to find massive moves that span days, binary options traders use it to predict the direction of the very next few candles.

Because binary options are fixed-time contracts, precision is everything. You do not just need to be right about the direction; you need to be right right now.

When I first started, I used to hunt for the best broker for learning price action because I realized indicators lagged too much for short-term expiration times. Price action operates on the foundation of market structure, which is divided into three distinct phases: bullish trending markets, bearish trending markets, and ranging or consolidating markets.

The Anatomy of a Bullish Trend

A bullish market structure is defined by a series of Higher Highs (HH) and Higher Lows (HL). When big buyers push the price up, it creates a peak (a high). When those buyers pause to take profits, the price dips temporarily, creating a trough. If the buyers step back in before the price falls past the previous low, they create a Higher Low.

For binary options, the absolute best time to take a “Higher” trade is not when the price is breaking out into a new Higher High. That is where beginners get trapped by sudden pullbacks. The golden entry is at the termination of a pullback, right as the asset forms its Higher Low.

The Anatomy of a Bearish Trend

Conversely, a bearish market structure consists of Lower Highs (LH) and Lower Lows (LL). Sellers drive the price down, take a breather, cause a minor upward retracement, and then slam the price down even lower.

If you are looking to place “Lower” trades, your eyes should be glued to the Lower Highs. Waiting for the price to bounce upward into a previous structural broken floor turned ceiling gives you the highest mathematical probability of winning a short-duration binary trade.

The Range: The Binary Options Trap

The third structure is the range, where the asset moves sideways between a relatively equal ceiling of resistance and a floor of support. While ranging markets can offer clean bounces if the channel is wide enough, tight ranges are highly toxic for short-term traders. I spent months learning how I learned to sit on my hands during choppy markets because attempting to trade a narrow range with 1-minute expiries is financial suicide.

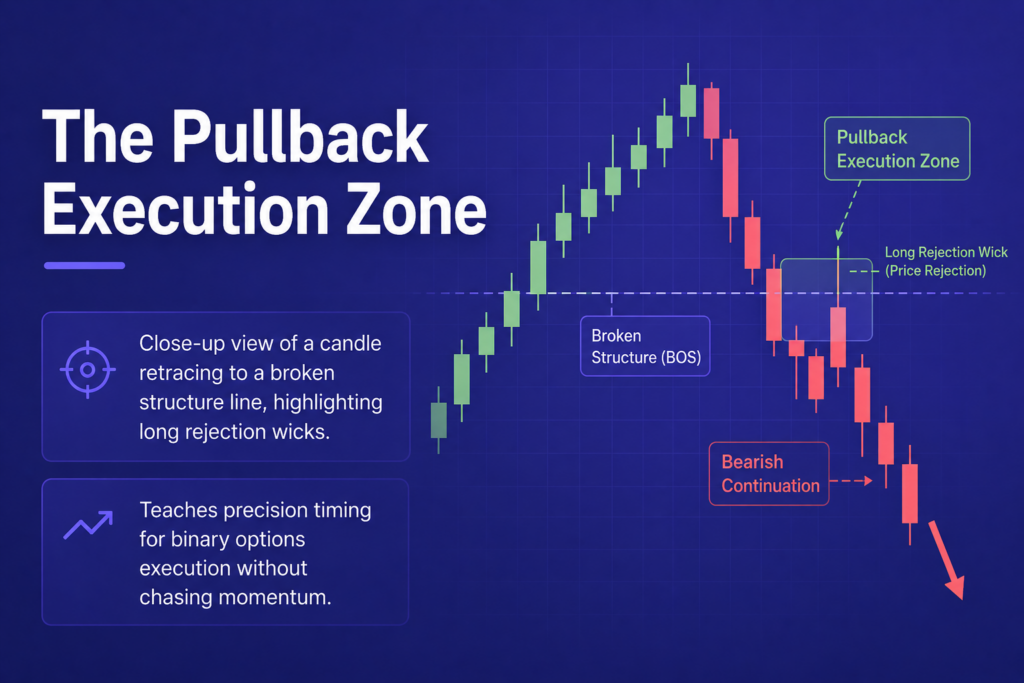

Reading Structural Shifts: The Break of Structure (BOS)

The real magic happens when you learn to identify when a trend is dying. A trend does not just stop out of nowhere; it gives clear architectural warning signs. This signal is known as a Break of Structure (BOS) or a Change of Character (CHoCH).

Imagine a bullish market that has been printing Higher Highs and Higher Lows consistently. Suddenly, the price rallies but fails to break above the previous Higher High. It prints a Equal High or a Lower High instead. Then, sellers aggressively push the price down, crossing clean through the last Higher Low.

The structural floor is broken. The bullish structure is officially dead, and a new bearish cycle has begun.

When I spot a Break of Structure on a clean platform like the IQ Option Platform, I immediately shift my bias. Instead of looking for buy entries, I wait for the price to retest that broken structural level from below to hunt for a high-probability sell trade.

Structuring Your Workspace for Short-Term Analysis

To trade market structure effectively, you do not need a screen cluttered with twenty different colorful lines. You need a platform that offers lightning-fast execution and highly responsive charting tools.

When I am testing out new strategies, I always check the safest trading platforms to ensure my charting lines stay exactly where I put them and don’t lag during high-volatility sessions. For traders who appreciate minimalism, finding a platform that doesn’t overwhelm you with unnecessary features is critical. Many beginners prefer reading pure price lines on a platform designed to be the best broker without complicated features to keep their psychological focus sharp.

Let’s look at how to map out a clear structural chart step-by-step:

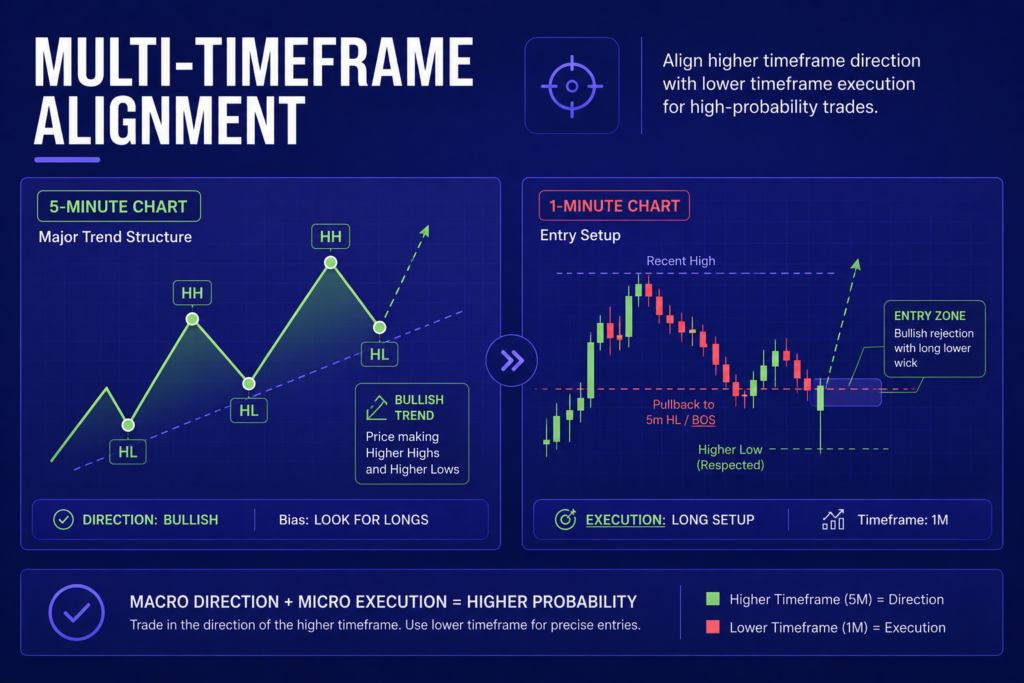

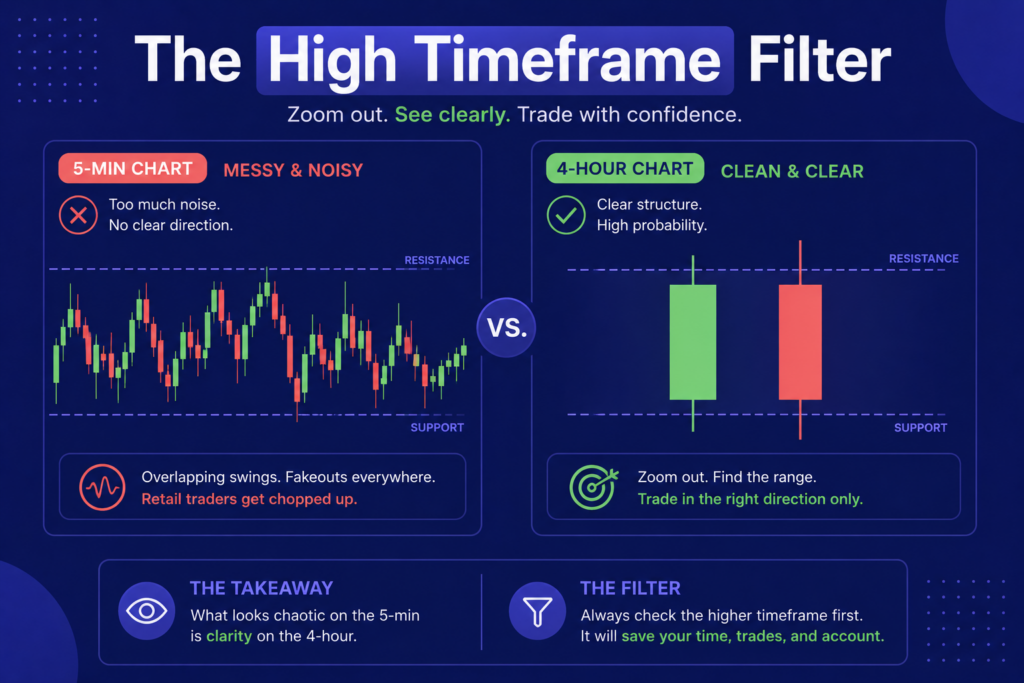

Identify the Master Trend on a Higher Timeframe: If you are trading 1-minute expiries, look at the 5-minute or 15-minute chart first. Is the overall market structure moving up or down? Always trade in the direction of the higher timeframe structure.

Mark Your Swing Highs and Swing Lows: Draw horizontal lines across the clear peaks and troughs on your chart. These represent the real battlegrounds of supply and demand.

Watch the Reaction at the Key Levels: When price approaches a previous structural point, do not guess. Look for candle rejection wicks. A long wick pointing downward at a Higher Low means the structure is holding, signalling a perfect moment to execute.

Practical Application Across Different Trading Ecosystems

Different brokers handle structural movements uniquely depending on their internal chart feeds and available assets. For instance, if you are looking to trade highly predictable, mathematically driven structures that run 24/7 without being affected by real-world news events, you might look toward synthetic assets. Many traders prefer the Deriv Platform for this specific reason, as its synthetic indices follow clean, algorithmic price action patterns beautifully.

If your style leans heavily toward trading traditional currency pairs during major sessions, you need rapid order fulfillment so you do not suffer from slippage at structural levels. For those who prioritize execution speed and clean interface mapping, exploring alternative options like the Pocket Option Platform, the Quotex Platform, or the highly responsive Expert Option Platform can make a substantial difference in catching volatile structural breaks.

Similarly, platforms like the Olymp Trade Platform and Capital Core offer excellent technical environments for drawing clear support and resistance lines across multi-timeframe structures.

Shifting From Gambler to Structural Master

The day I stopped guessing whether the next candle would be green or red was the day I finally started treating binary options like a real business. It requires patience. It requires you to sit on your hands and wait for hours if necessary until the price arrives exactly at a verified structural zone.

If you are tired of watching your hard-earned capital vanish due to unpredictable market swings, it is time to stop trading blindly. You need deep analytical insights, precise daily forecasts, and a community that decodes the real movements behind the scenes.

To truly take your market comprehension to an institutional level, check out the specialized insights available at the Becoin Forecast Hub and step up your game by securing your access to the Becoin Premium Tariff Plan. Do not let the market dictate your financial future; learn its structure, read its blueprints, and take control of every single trade you make.

How I Learned to Sit on My Hands During Choppy Markets

I remember the morning vividly. It was a Tuesday. The coffee on my desk was still piping hot, the charts on my screen were blinking, and I was feeling incredibly confident. I had just finished reading about how market open hours create the best trading opportunities, and I was ready to hunt for a clean setup.

My favorite currency pair had been in a beautiful, clean uptrend for three consecutive days. It was a textbook setup. I expected a minor pullback to a key support level, followed by a strong bounce back to the skies.

Instead, I stepped directly into a meat grinder.

The price hit my level, and I bought. Almost instantly, the market reversed and knocked out my stop-loss. I shook it off. It happens. Loss is part of the game. I waited a few minutes, noticed a massive bearish engulfing candle, and decided to flip my bias. I went short. Two minutes later, the market aggressively spiked upward, taking out my second stop-loss.

Frustration started to warm up the back of my neck. I adjusted my indicators, looked closely at the screen, and placed a third trade. Wipeout. Within forty-five minutes, I had lost two weeks’ worth of hard-earned profits. The market wasn’t trending up, and it wasn’t trending down. It was violently jerking back and forth in a tight, unpredictable twenty-pips range. It was a choppy market.

That day, I didn’t just lose money. I lost my emotional balance. It took me months to realize that the problem wasn’t my technical strategy or my indicators. The problem was my lack of situational awareness. I was trying to use a map meant for a highway while driving through a swamp.

Here is what I learned from that painful experience, and how you can save your account from the slow, agonizing death of a thousand cuts that sideways markets love to inflict.

Understanding the Beast: What is a Choppy Market?

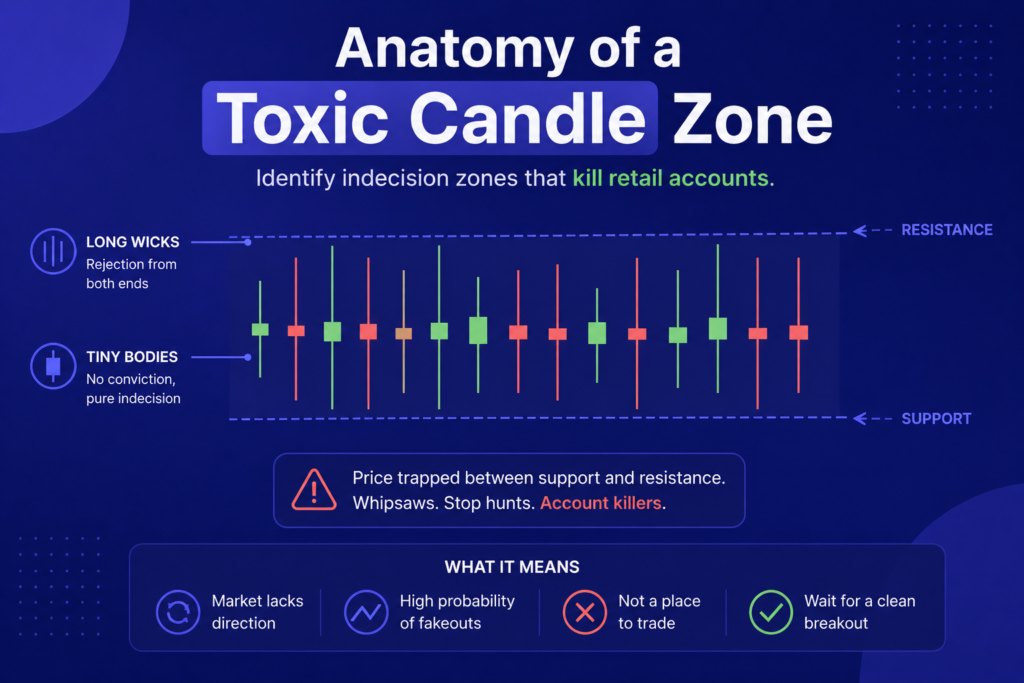

Before you can avoid a choppy market, you have to recognize it. In simple terms, a choppy market occurs when the price moves sideways in a highly erratic fashion without any clear direction. Unlike a healthy ranging market, where the price bounces smoothly between a defined support floor and a resistance ceiling, a choppy market breaks minor levels constantly, prints long wicks on both sides of the candles, and mimics breakouts only to fail immediately.

It is a state of equilibrium driven by indecision. Big institutional players are either sitting on the sidelines or actively accumulating positions without pushing the price out of its current zone.

When you look at your dashboard during these times, everything looks messy. If you are using a platform known for having the cleanest interface real comparison for beginners in 2026, the messiness becomes even more glaringly obvious because the candles will look fragmented and chaotic.

The primary trap here is psychological. As retail traders, we are conditioned to believe that more activity equals more profit. We look at the moving tickers and feel an overwhelming urge to participate. But in a choppy environment, participation is exactly what the market wants because it feeds on your transaction fees and your stop-losses.

The Signs I Missed: Identifying Choppiness Early

I used to think that identifying a choppy market was something you could only do in hindsight. I was wrong. The market leaves subtle clues at the very beginning of a sideways phase.

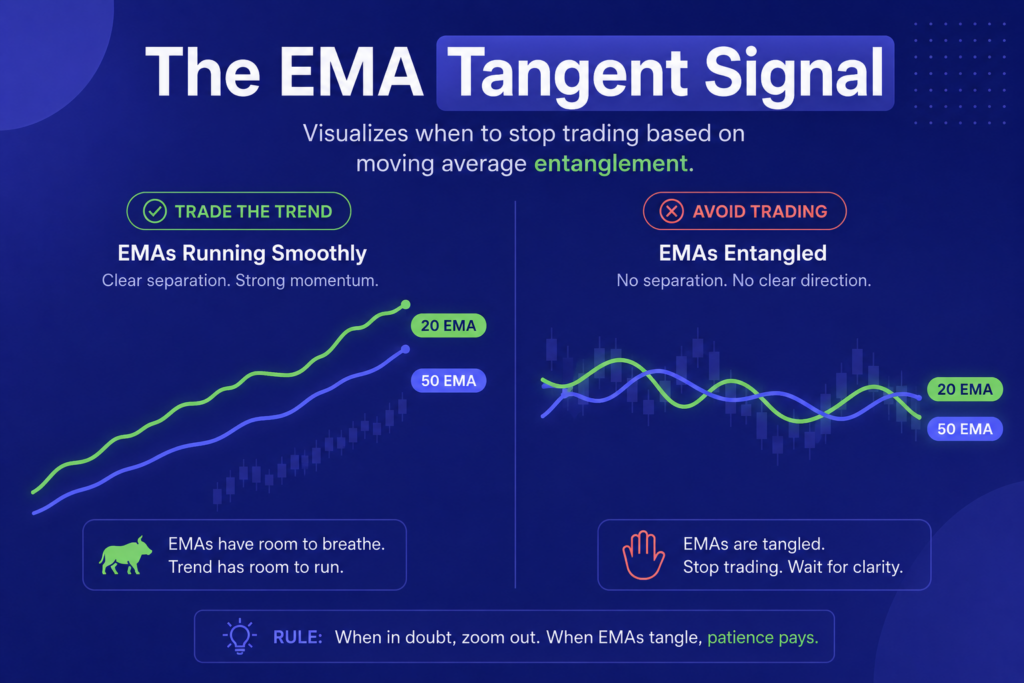

First, watch the moving averages. If you use a simple tool like a 20-period and a 50-period exponential moving average (EMA), look at how they interact. In a strong trend, they run parallel to each other, acting as dynamic support or resistance. In a choppy market, they start to flatten out and repeatedly cross over one another like a tangled ball of yarn. When the price begins to weave through your moving averages like a slalom skier, step away from the order button.

Second, pay close attention to candle wicks. If you see consecutive candles with small bodies and long wicks pointing both up and down, it means neither buyers nor sellers are controlling the narrative. It is a violent tug-of-war where both sides are losing strength.

If you want to practice spotting these structural shifts without risking a large sum of money, it is highly recommended to use a platform that accommodates micro-investments. You can read my breakdown on the best broker for $10 deposit tested platforms 2026 to see where you can safely test your market-reading skills.

The Mental Trap of “Recouping Losses”

The most dangerous part of a choppy market isn’t the initial loss. It is the emotional spiral that follows. When I lost those first two trades on that fateful Tuesday, my logical brain went completely dark. A dark, vengeful entity took over my hands. I wanted my money back, and I wanted it immediately.

This is why 90% of traders lose money real reasons beginners don’t realize. They don’t understand that the market doesn’t owe them a single dime. When you lose money in a sideways market, your immediate instinct is to tighten your stops or increase your lot size to win it back in one single shot. In a choppy environment, a tighter stop-loss just means you will get stopped out even faster.

I remember staring at my screen, watching the balance drop, and wondering if my execution app was lagging. I even questioned if my internet connection was causing bad fills. If you ever feel like your technical setup is working against you, it helps to check if you are using the best trading platform for slow internet in 2026 to eliminate technical variables from your frustrations. But let me be entirely honest with you: most of the time, it isn’t the internet. It is the choppy price action playing tricks on your mind.

Your Survival Guide: Concrete Rules for a Sideways Market

Over the years, I developed a strict set of personal rules that keep me safe when the charts start looking erratic.

First, I implemented a “Two Strikes and Out” rule. If I take two consecutive losses in a single trading session, I close my charts immediately. I don’t look at my phone, I don’t check my open PnL, and I don’t try to find a “perfect” setup to break even. Two losses mean either my analysis is wrong, or the market conditions are completely unplayable. In both scenarios, staying active is a losing proposition.

Second, I learned to track session volume. Choppiness often occurs during the transition periods between major global financial sessions. If you study the clock and the cash my journey into the hidden rhythm of session based trading, you will notice that the market frequently dries up right after the London session closes and before the New York afternoon volume kicks in. Trading during these dead zones is an absolute recipe for account destruction.

Third, change your perspective by shifting to a higher timeframe. If the 5-minute chart looks like an irregular heartbeat, zoom out to the 1-hour or the 4-hour chart. Frequently, you will realize that what looked like a massive breakout attempt on the lower timeframe is actually just a tiny, insignificant wick on a higher timeframe candle. Zooming out grounds your perspective and prevents you from chasing ghosts.

For those who prefer a highly systematic approach, choosing platforms that offer robust analytical layouts can make a massive difference. You can read a direct head-to-head analysis on the IQ Option vs Deriv chart comparison to see which interface gives you a clearer view of high-level trends versus low-level noise.

The Power of Doing Absolutely Nothing

It takes a massive amount of discipline to look at a live chart and decide to do absolutely nothing. We live in a world that rewards constant hustle and endless productivity. In trading, the opposite is frequently true. Sometimes, the most profitable action you can take is to close your laptop, walk outside, and preserve your capital for a day when the market is ready to cooperate.

When you protect your capital during bad market conditions, you ensure that you still have money to trade when beautiful, high-probability trends return. Think of your account balance as your ammunition. If you waste all your bullets shooting at shadows in the dark, you will have nothing left when the target finally walks out into the clear daylight.

If you are currently looking for a reliable, heavily tested environment to build your skills and manage your trades during clean market conditions, it is vital to pick platforms with a proven track record. For beginners starting out with smaller balances, exploring the options available via the IQ Option platform can provide a highly stable starting ground. Alternatively, you can explore the features of the Binomo trading portal to see if its execution flow aligns better with your personal pace. For a detailed breakdown of how these specific ecosystems stack up against each other regarding execution speed and entry requirements, don’t miss my analysis on which is easier for beginners Binomo or IQ Option.

Upgrading Your Edge

Learning to sit on your hands during low-volume, erratic environments changed my career entirely. It was the day I stopped trading and finally started making money. But discipline is only half the battle. The other half is access to institutional-grade insights that help you anticipate these bad market phases before they destroy your balance.

If you are tired of guessing whether the market is starting a clean breakout or entering a deadly trap, you need to elevate your analytical toolkit. By joining the BeCoin Premium Membership, you gain access to institutional-grade, predictive data streams and direct access to the BeCoin Forecast Hub. Stop gambling against algorithms in the dark. Protect your capital, master your emotional baseline, and trade with a definitive structural edge.

Why Market Open Hours Create the Best Trading Opportunities

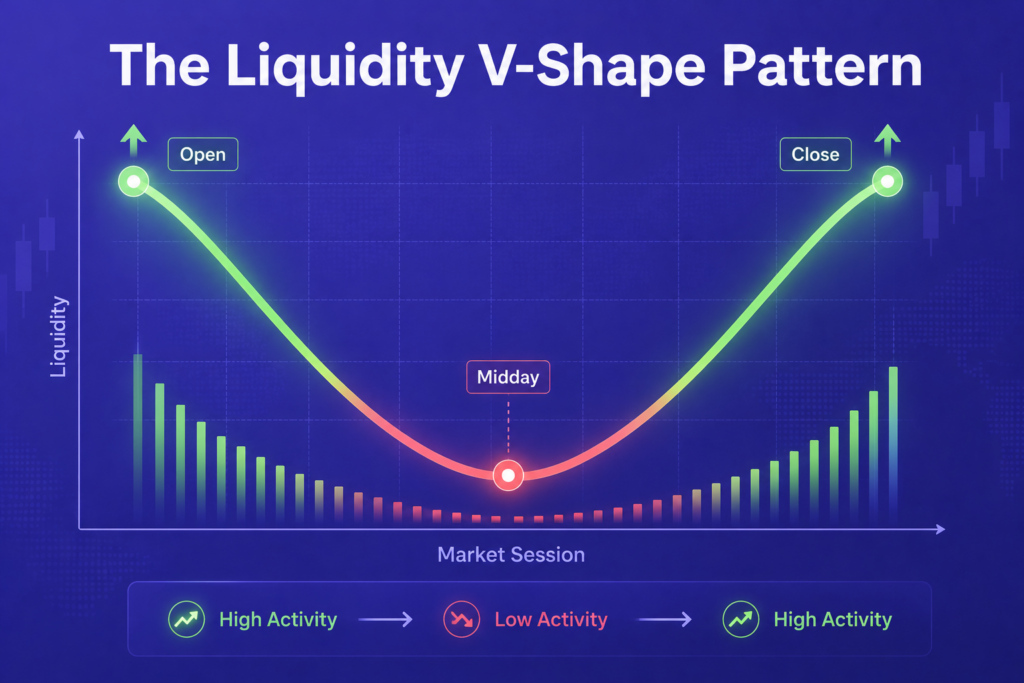

I used to think trading was a 24-hour conveyor belt of endless cash. In my earliest days, armed with a laptop, a hot cup of coffee, and far too much unearned confidence, I would stare at charts at 11:00 PM on a Tuesday. The candles barely moved. They crawled across my screen like snails on a sleepy afternoon. I would force trades out of sheer boredom, trying to squeeze profit out of microscopic price wiggles, only to get eaten alive by spreads and sudden, random reversals.

It took losing a painful amount of capital to realize a fundamental truth about the financial markets: the market does not care about your work schedule. It has its own heartbeat, its own opening bell, and its own rush hours.

When I finally figured out that the highest concentration of trading opportunities happens during specific market open hours, my entire approach shifted. I stopped chasing the market and started waiting for it to wake up. Here is the raw story of how I learned to ride the opening waves, why these hours hold the highest win potential, and how you can structure your day to exploit them.

The Ghost Town vs. The Trading Floor

Imagine walking into a massive shopping mall at 4:00 AM. The lights are dim, the doors are locked, and the only sound is the echo of your own footsteps. If you wanted to sell a high-end watch right there, your chances of finding a buyer are close to zero. If you do find someone, they will probably offer you pennies on the dollar because there is no competition.

That is what trading feels like during the dead zones—those awkward transition hours between the close of New York and the slow awakening of Sydney and Tokyo.

Now, imagine that same mall at 10:00 AM on a Saturday. The doors fly open, thousands of shoppers stream in, music is playing, and buyers are actively competing for goods. Prices move rapidly, transactions happen in milliseconds, and the energy is palpable.

In the digital markets, the opening bell of a major global session—be it London, New York, or Tokyo—is that Saturday morning rush.

When a major market opens, institutional investors, hedge funds, algorithmic bots, and retail traders all dump their orders into the order book at the exact same time. This massive influx creates two beautiful ingredients that every successful trader needs: extreme liquidity and explosive volatility. Without these two, you are essentially trying to sail a boat in a puddle with no wind.

The Magic Magic Hour: The London and New York Overlap

If you want to know the exact moment my trading account turned a corner, it was when I synchronized my alarm clock with the overlap of the London and New York sessions.

The London session opens early in the morning European time, bringing in the massive weight of European banking capital. A few hours later, New York traders wake up, pour their coffee, and open their terminals. For roughly a four-hour window, the two largest financial capitals on earth are trading simultaneously.

The sheer volume during this overlap is staggering. Trends do not just form; they accelerate. Support and resistance levels that held firm for twelve hours suddenly shatter as institutional momentum drives prices toward clean targets.

Before I realized this, I spent months analyzing charts during quiet periods, wondering why my perfect technical setups kept failing. The answer was simple: there was no volume to push the price through the levels. Understanding this structural reality is why many traders end up migrating across platforms, looking for environments that handle high-velocity execution smoothly. If you have ever wondered why execution speed matters so much during these frantic windows, you can read more about why traders move from Binomo to Deriv in 2026 for a clearer perspective on platform mechanics.

During the open, the spread—the difference between the buy and sell price—shrinks to its narrowest point because there are so many participants. This saves you money the second you click “Buy” or “Sell.” More importantly, the price action becomes highly predictable because it is driven by real directional intent, not random retail noise.

Why the First 60 Minutes Dictate the Whole Day

There is a distinct psychological phenomenon that happens during the first hour of a market open. I call it the “unzipping” of the market.

Overnight, while a specific market was closed, world events kept happening. Companies released earnings, politicians made announcements, and economic data dropped. Because the local exchange was closed, all that raw human emotion and fundamental data got compressed into a coiled spring.

When the opening bell rings, that spring uncoils instantly.

The first hour is a battlefield where the market plays catch-up. You will often see a massive initial spike in one direction, followed by a sharp reversal as early trapped traders get liquidated, followed finally by the true trend of the day establishing itself.

Early on, I used to jump into the market the exact second the clock struck the opening hour. It was an adrenaline rush, but it was also financial suicide. I was getting chopped up in the initial chaos.

Eventually, I adapted my strategy. I began to treat the first fifteen to thirty minutes as an observation window. I let the big institutional players battle it out, let the initial volatility clear out the weak hands, and then I looked for clean price action entries once a clear direction emerged. This patient, methodical approach completely transformed my daily routine. If you are struggling to find a balance between your personal life and the chaotic market schedule, exploring my personal journey in finding my perfect workspace and building a daily trading routine might give you some practical structural ideas.

Matching the Session to Your Trading Identity

One of the biggest mistakes I see beginners make is trying to trade every single session with the exact same strategy. They will use an aggressive breakout strategy during the quiet Asian session, or a slow range-bound strategy during the explosive New York open. It never works.

Every market session has a completely unique personality, and your strategy must match that personality.

The Tokyo/Asian Open: This session is traditionally calmer, more deliberate, and prone to consolidation. It is a fantastic environment for mean-reversion strategies, where you trade the bounces off well-defined support and resistance ranges.

The London Open: This is the trendsetter. London loves to break out of the ranges established overnight during the Asian session. If you love trading explosive breakouts and high-momentum line breaks, this is your playground.

The New York Open: This is the wild card. It brings immense volume but is heavily influenced by macroeconomic news events, interest rate decisions, and employment data releases. It requires sharp risk management because reversals can be swift and violent.

To navigate these personality shifts, you need platforms that do not choke when the volume spikes. If you are operating with a smaller retail bankroll, choosing the right venue is critical. I highly recommend looking over the comprehensive analysis of Binomo vs IQ Option for small accounts to see which ecosystem provides the stability you need when a session kicks off.

The Dark Side of the Open: Managing the Chaos

I would be lying if I said the market open is an easy ticket to wealth. The same volatility that creates massive profit windows can wipe out an undisciplined account in seconds.

When the volume surges, slippage can happen. You might click to enter a trade at one price, but because the market is moving at terminal velocity, your order gets filled a few pips away. If your platform has poor charting tools or lagging execution, you are starting the race with a broken leg.

To survive the open, your risk management has to be completely automated and entirely unemotional. I never enter an opening bell trade without a hard stop-loss already calculated and plugged into the system. The market moves too fast for mental stop-losses; by the time your human brain processes that a trade has gone wrong, your balance could take a catastrophic hit.

Finding tools that allow you to manage this risk cleanly is a vital part of your development. For a deeper look at platforms built to protect your capital during high-velocity moves, take a look at the breakdown of which broker has better risk management tools.

The Real Cost of Forcing Trades in the Dead Zones

It took me years to realize that some of the highest-earning days I will ever have are the days where I simply choose not to trade.

When you try to trade outside of the market open hours, you are essentially gambling against the house edge. The lack of volume means the market is easily manipulated by single large orders. You will see a candle spike up, convince yourself a trend is starting, buy in, and then watch the price immediately collapse because there was no genuine institutional follow-through behind the move.

When I shifted my focus exclusively to the primary session opens, my stress levels plummeted. I no longer had to sit at my desk for twelve hours a day, frying my nervous system. Instead, I spend two to three highly focused hours trading the open, and then I close my laptop. I let the market do the heavy lifting while I go live my life.

If you are currently trapped in the loop of constant, exhausting overtrading, you are not alone. It is a phase almost every professional trader goes through before they learn the value of timing. You can read my candid personal reflection on the day I stopped trading and finally started making money to see exactly how stepping back can miraculously push your account forward.

Stepping Up to Professional Execution

If you are ready to stop treating the markets like a casino and start trading the sessions with institutional precision, you need to use platforms designed to handle high-volume opens without lagging or freezing.

For fast-paced binary and digital options strategies where every single second counts on the execution clock, I highly recommend opening an account with IQ Option. Their charting engine is highly intuitive and exceptionally fast. If you want a platform known for seamless navigation and smooth asset transitions during heavy volume shifts, take a look at Binomo to see how it fits your routine.

For traders who prefer exploring non-traditional assets, algorithmic setups, or unique market instruments during global session handoffs, checkout the specialized trading environments over at Deriv, experiment with the lightning-fast fills at Pocket Option, or test the sleek operational agility provided by Quotex. If you are looking for straightforward platforms tailored for crisp execution layouts, look into ExpertOption or explore the institutional-grade routing tools available at Capital Core.

Gain the Ultimate Edge with Becoin Premium

Understanding the clock is only the first step to financial independence. Knowing exactly what to do when that clock strikes the hour is what separates the top ten percent of traders from the ninety percent who consistently wash out their accounts.

You do not have to sit in front of the charts guessing where the big institutional money is moving next. By joining our inner circle, you get access to institutional-grade market depth, real-time volume analysis, and predictive session breakdowns before the opening bell even rings.

Stop fighting the tide alone. Give your strategy the professional structural backing it deserves. Join Becoin Premium today and start trading with an unfair analytical edge.

The Clock and the Cash: My Journey into the Hidden Rhythm of Session-Based Trading

There was a time when I thought the global financial market was a single, monstrous wave that never stopped moving. I believed that if I sat in front of my monitors long enough, clicking buttons whenever a pretty pattern appeared on my charts, the market would eventually reward my sheer endurance.

I was dead wrong.

During my first year, I spent thousands of hours staring at candles, completely blind to the macro reality that the market is not a singular entity. Instead, it is a sequential passing of the torch from Tokyo to London, and finally to New York. Each region has its own personality, its own traps, and its own unique rhythm.

If you are currently struggling to find consistency, let me ask you a question that completely shifted my career: Are you trading a strategy that actually fits the specific hour on your clock?

When I finally stopped treating the market like a 24-hour casino and started adjusting my execution to match the Asian, London, and New York sessions, my results completely transformed. This is the raw story of how I learned to navigate the specific micro-climates of the trading day, and how you can use these rhythms to stop blowing accounts.

The Sleepless Traps of a 24-Hour Market

My journey into session-based trading started out of absolute desperation. I remember sitting at my desk at 2:00 AM, exhausted, watching the price of EUR/USD move by a mere three pips over the course of two hours. Frustrated by the lack of movement, I would artificially increase my position size just to make the trade “interesting.” Inevitably, the market would experience a tiny spike, hunt my over-leveraged stop loss, and leave me sitting in the dark with less money than I had at midnight.

That period of my life taught me a brutal lesson. If you do not understand who is controlling the order flow at any given minute, you are essentially trading with a blindfold on. I was falling directly into the traps that wipe out most newcomers. If you want to know more about those early structural errors, you should read about why 90 percent of traders lose money. It took me a long time to realize that success is not about trading more often; it is about trading when the odds are stacked in your favor.

The global market runs on structural liquidity. Central banks, commercial conglomerates, and institutional hedge funds do not operate at random times. They follow standard business hours. When Tokyo opens, Asian corporations manage their capital. When London wakes up, the massive European institutions flood the market with volume. When New York enters the fray, the highest concentration of financial capital on earth collides with Europe.

Once I mapped out these specific transitions, my perspective changed completely. I stopped hunting for trades during dead hours and started waiting for the structural expansions that define the major shifts in the global clock.

The Silent Architect: Mastering the Asian Session

The Asian session is often treated as an afterthought by retail traders because it lacks the explosive, chaotic volume of the Western sessions. For the longest time, I completely ignored it. I assumed nothing of value happened while Europe and America slept.

I was missing the entire foundation of the trading day.

The Asian market, primarily anchored by Tokyo, Sydney, and Singapore, behaves like a consolidation machine. Because institutional volume is significantly lower during these hours, prices tend to stay contained within tight, predictable structural ranges. Instead of massive, sweeping trends, you see orderly support and resistance levels holding firm.

When I started practicing on clean setups, I realized that this specific time window is a fantastic environment for anyone focusing on highly disciplined, lower-vulnerability strategies. If you want to refine your execution without getting whipped out by sudden news events, it helps to use platforms designed for clean data delivery. For instance, you can test these steady ranges by starting a practice account on IQ Option or exploring the streamlined layout of Binomo.

The real secret of the Asian session is not just about trading inside the range; it is about realizing that this range defines the landscape for the rest of the day. The highs and lows set during the Asian hours become massive targets for institutional algorithms when London opens. Institutional money loves to sweep the liquidity resting just outside the Asian boundaries. By observing how price behaves inside this initial block, I learned to anticipate exactly where the market would hunt for liquidity later in the morning.

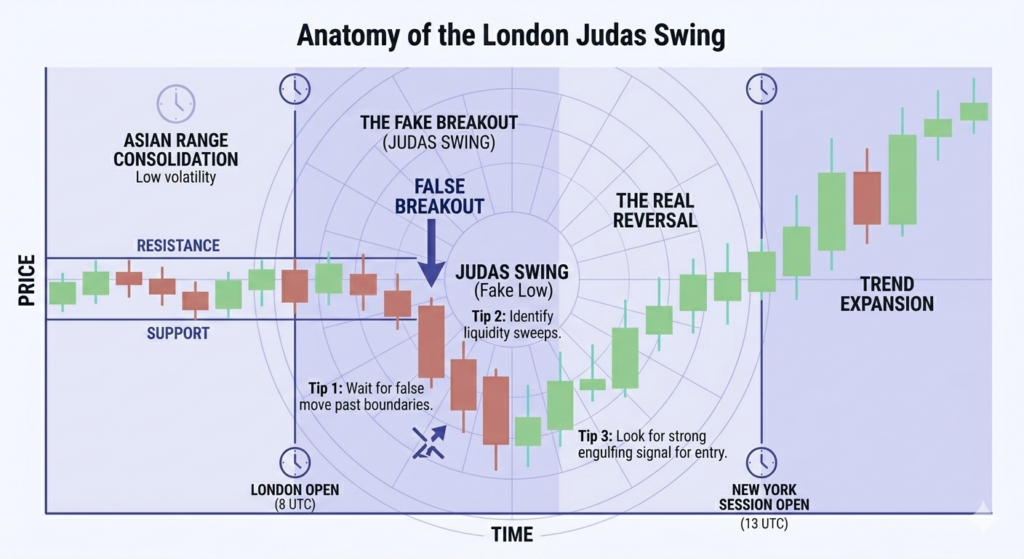

The Volatility Explosion: Navigating the London Open

If the Asian session is the silent architect, the London open is the wrecking ball. The shift between these two periods was the hardest transition for me to learn, and it cost me a significant amount of capital before I finally understood its mechanics.

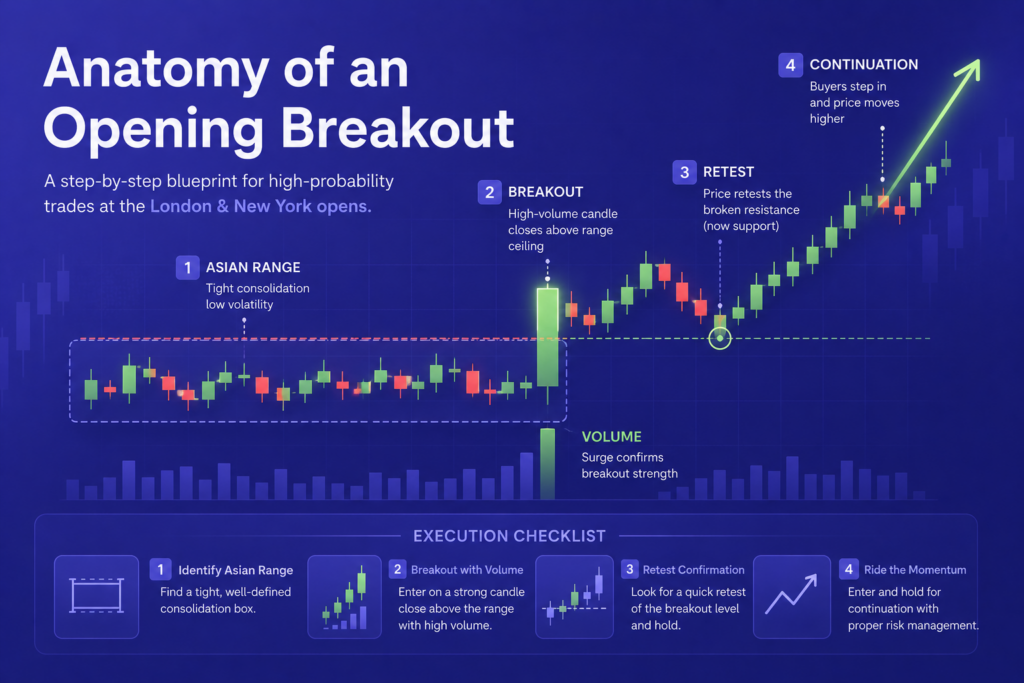

Picture this: London traders sit down at their desks, look at the tight range formed during the Asian hours, and immediately begin executing massive blocks of orders. Within minutes, volume surges exponentially. Price aggressively breaks out of the Asian range, making it look like a massive trend is forming.

Early in my career, I would eagerly jump onto these initial breakouts, convinced I was catching the wave of the day. Without fail, the price would violently reverse, clear out my stop, and accelerate in the completely opposite direction.

I was falling victim to the classic London Judgments Trap, frequently referred to as the “Judas Swing.” Institutional algorithms deliberately push price past the Asian highs or lows to trigger retail stop losses and collect liquidity. Once those stops are cleared, the true trend of the London session begins.

Once I understood this manipulation, my strategy flipped. I stopped buying the immediate breakout. Instead, I waited for London to sweep the Asian session boundaries, watched for a clear structural failure, and then entered the market alongside the real institutional flow.

This specific window requires split-second execution and deeply reliable order fills. When you are navigating that level of rapid price movement, having a platform with a seamless UI is non-negotiable. If you are analyzing these rapid breakouts, finding a setup with a highly responsive workspace is essential for your sanity. I spent a long time looking for the right fit, which I detailed in my personal journey toward finding my perfect trading workspace.

The Crossover Chaos: When London Meets New York

The absolute peak of the trading day occurs during the London and New York overlap. This window represents the highest concentration of financial liquidity on earth. For roughly four hours, the world’s two largest financial centers are operating simultaneously.

The market during the overlap is a different beast entirely. Volume skyrockets, trends become highly aggressive, and macroeconomic news releases out of Washington dump massive amounts of volatility into the charts within milliseconds.

During this phase, any structural weakness in your execution or your broker will be instantly exposed. Slippage can widen, spreads can fluctuate, and emotional decisions will destroy an account faster than you can blink. I quickly realized that attempting to trade the crossover without a concrete, tested strategy is financial suicide.

To survive this period, I had to develop absolute clarity on my risk limits. I learned to identify my key institutional levels before the overlap even started. If the market did not hit my specific entries, I simply stood aside.

Because the crossover moves so quickly, having an optimized technical environment is just as important as your analytical skills. If your charts lag or your platform hitches for even a second during a major New York data release, your trade is compromised. For high-volume environments, choosing a system built for low-latency data processing is critical. You can look into specialized options like Deriv for synthetic or underlying assets, or utilize reliable standard environments like Pocket Option and Quotex to manage your active trade execution.

Designing a Sustainable Daily Trading Routine

The ultimate goal of understanding session-based trading is to build a lifestyle that does not require you to sit in front of a computer screen for twelve hours a day. When I stopped trying to trade every single session and picked a single timezone to master, my profitability stabilized, and my mental health returned.

Today, my routine is highly structured. I wake up during the latter half of the Asian session to observe the established structural boundaries. I do not take trades here; I simply map out the sandbox. When the London session opens, I watch for the inevitable liquidity sweeps. If a clear price action model presents itself, I take my trade, manage my risk aggressively, and close my laptop.

If you are a student or balancing a full-time corporate job, this session-based approach is the only way to trade without losing your mind. You do not need to watch the screen all day. You simply need to allocate one or two hours of focused attention during a major session open. For those trying to balance limited hours and capital, selecting a highly accessible partner is a great first step. You can read my breakdown on which broker is better for students to see how to align your lifestyle with your chosen market hours.

Your Next Steps in the Markets

Mastering the clock requires patience, intentional practice, and the right environment to execute your ideas without unnecessary friction. Do not try to conquer all three sessions tomorrow morning. Pick the one that naturally aligns with your waking hours, study its unique structural traps, and focus on mastering that single window of time.

If you are currently looking for a place to practice these session transitions with real-time data, you can set up a basic profile on ExpertOption or look into the alternative features provided by CapitalCore. Take the time to find an interface that keeps your analysis clean and clear.

The market will always be there, but your capital will not if you continue to trade at random hours without a structural plan. Stop treating the market like an unpredictable wall of noise. Respect the global clock, map out your sessions, and protect your capital at all costs.

If you are tired of guessing where the next institutional liquidity sweep will occur and want to fast-track your path to consistency, you need a deeper layer of market analysis. Join our private community at BeCoin Premium Tariff Plan to gain access to comprehensive daily session breakdowns, real-time institutional volume tracking, and advanced price action strategies that give you a definitive edge in the markets. Let’s stop guessing and start trading with professional precision.

The Clock and the Candle: How I Stopped Guessing the Best Time to Trade Binary Options