Capital Core Verification Process Explained: KYC, Restrictions, and Withdrawal Delays

I learned something the hard way with offshore-style brokers: the smoothest part is usually opening the account, funding it, and placing the first few trades. The real test starts when you try to move money back out.

That’s exactly why I wanted to document the Capital Core verification process from a trader’s perspective, not from a generic FAQ angle. When I first looked into Capital Core, I found plenty of pages talking about deposit methods, bonuses, account types, and trading features. What I didn’t find enough of was the part that actually matters once real money is involved: KYC timing, withdrawal restrictions, payment method matching, regional limitations, and what causes delays when you finally hit the withdrawal button.

That gap matters because most traders do not lose confidence during registration. They lose confidence during withdrawal.

So this is my practical, experience-driven breakdown of how I think about the Capital Core verification process, what I’ve observed from traders, and what I would personally do to reduce the chance of getting stuck between “withdrawal requested” and “withdrawal completed.”

If you’re planning to test the platform with a small amount first, that’s exactly how I’d approach it too. You can open a low-risk starter account here and treat your first deposit like a live systems test, not a commitment: Open a Capital Core account here

Why I Started Taking Verification More Seriously Than Strategy

Early on, I used to focus almost entirely on entries.

Was EUR/USD rejecting a level?

Was the candle structure clean?

Was there enough momentum to justify the risk?

But after a few years of trading across different brokers and platforms, I realized something uncomfortable: a profitable trade means very little if the cash-out process is unclear.

That’s why I now treat broker testing in three layers:

- Platform execution

- Funding and account rules

- Verification and withdrawals

If layer three is weak, the rest is noise.

With Capital Core, the marketing is easy to understand. The harder part is understanding the real-world flow of the Capital Core verification process:

- Can you deposit before full KYC?

- When does verification become mandatory?

- What documents do they actually want?

- Why do some withdrawals get held for review?

- Can you withdraw to a different method?

- What happens if your country or payment route gets flagged later?

Those are the questions most “review” pages skip. That’s the content gap I wanted to close here.

My First Realization: You Can Deposit Before Full Verification, But That Doesn’t Mean You’re Ready

One of the first things I noticed is that Capital Core allows some traders to fund an account before completing full verification, depending on the payment method. That sounds convenient on the surface.

But from a trader’s perspective, this is where a lot of people make their first mistake.

They think:

- “My deposit worked”

- “The platform let me trade”

- “So I’m good”

No. You’re not good yet.

You’re only funded, not fully operational.

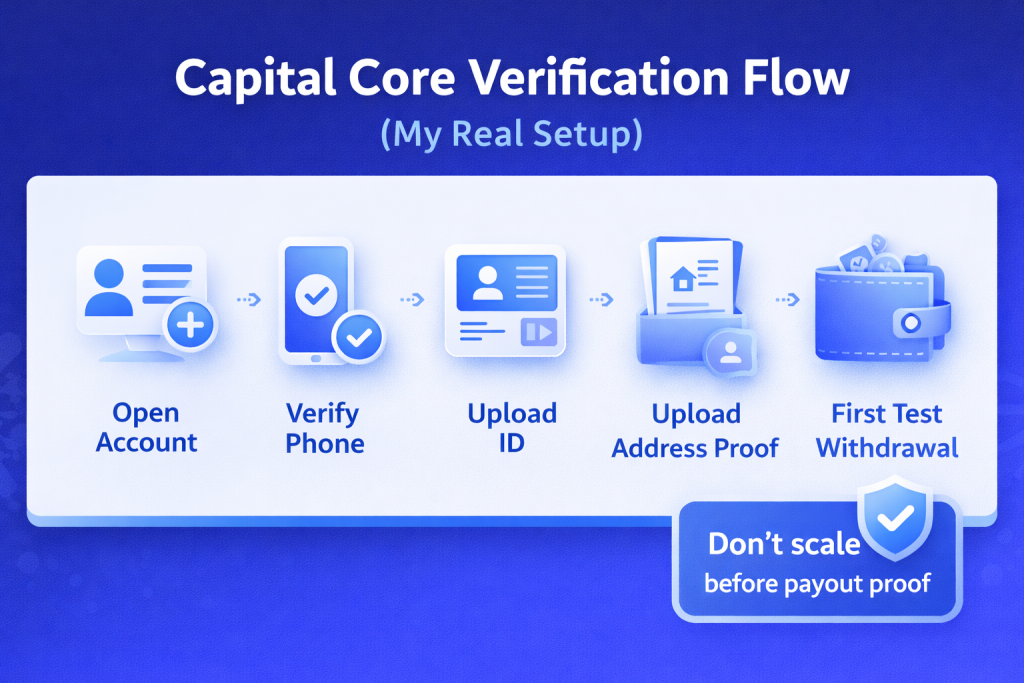

That distinction is critical. If I’m using Capital Core, I do not consider the account “usable” until these are done:

- Identity verified

- Address verified

- Phone verified

- Preferred withdrawal method understood

- First test withdrawal completed

That’s my actual standard now.

Because the broker letting you trade before full verification is not the same as the broker being ready to release your money later.

If you’re starting with a small balance, I’d also read whether a $10 Capital Core account is actually usable before you fund anything meaningful.

What the Capital Core Verification Process Actually Looks Like

From everything I’ve seen, the Capital Core verification process follows the standard KYC and AML framework you’d expect from a broker operating in this space:

- Identity verification

- Address verification

- Phone verification

- Ongoing account activity monitoring

- Payment method ownership checks

- Same-name and same-source funding rules

That tells me a few things immediately.

1) KYC is not just a one-time upload

A lot of traders think KYC ends when the document says “approved.” In practice, it often doesn’t.

The real-world version of this is simple:

- unusual deposit or withdrawal patterns,

- sudden larger payouts,

- new payment methods,

- location mismatches,

- or account behavior that triggers internal review

can all bring your account back under extra scrutiny.

2) The payment method is part of your KYC

This is where many traders get caught.

If you deposited with one route and later try to withdraw somewhere else, you’re no longer just making a withdrawal request. You’re creating a compliance event.

3) Country risk can change the intensity of review

If your jurisdiction is considered higher-risk under internal AML rules, your verification may not be “one and done.” Additional checks can happen later, especially around withdrawals.

That’s not unique to Capital Core, but it matters more on platforms where traders often use e-wallets and crypto.

If you’re based in the U.S. or writing for U.S.-based readers, it’s worth pairing this with my breakdown of whether Americans can use Capital Core safely, because regional rules can change the whole experience.

The Documents I’d Prepare Before I Ever Place a Real Trade

If I were walking someone through the Capital Core verification process as a private checklist, this is exactly how I’d do it.

My pre-trade verification checklist

| Verification area | What I’d prepare | Why it matters |

| Identity | Passport, national ID, or driver’s license | Confirms legal identity and name match |

| Address | Utility bill, bank statement, or government letter | Confirms residence and jurisdiction |

| Phone | Working number that can receive SMS or calls | Needed for account security and possible manual verification |

| Payment method ownership | Same name on PayPal/e-wallet/crypto account where possible | Reduces payment mismatch risk |

| Deposit proof | Screenshots or transaction IDs | Useful if support asks for proof later |

| Withdrawal route | Decide it before depositing | Prevents “different method” delays |

The phone part deserves more attention than most traders give it.

I’ve seen traders ignore phone verification until there’s a problem, then suddenly support needs to reach them and the number isn’t reliable.

That is not where I want friction.

If your phone number is weak, unreachable, VoIP-only, or inconsistent with your country profile, you’ve created a future problem before your first trade.

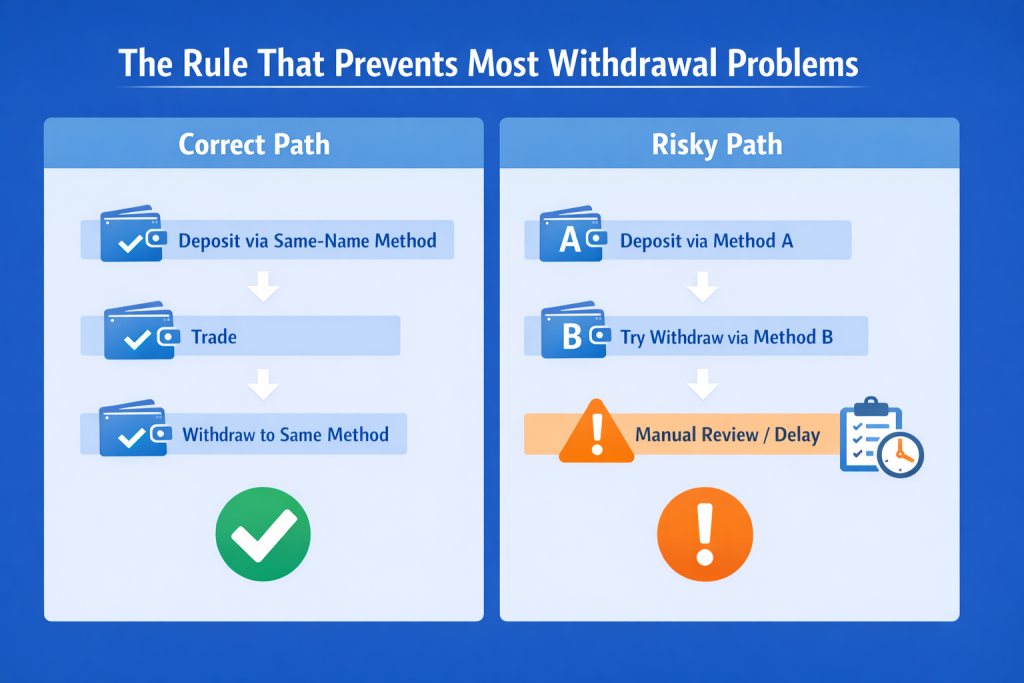

The Restriction Most Traders Miss: Same Deposit Method, Same Account Name

This is the single most important operational rule in the Capital Core verification process.

From a practical standpoint, the logic is simple:

- funds should come from an account under the same name as the trading account,

- third-party funding is risky territory,

- withdrawals usually work best when they go back through the same method as the deposit,

- and the account used for withdrawal should match the original funding path.

This is not a small footnote. This is the rule that explains a huge percentage of “my withdrawal is delayed” stories across brokers.

Here’s the mistake pattern I’ve seen many times:

- Trader opens account quickly

- Deposits using the easiest available method

- Starts trading without planning the exit route

- Makes profit

- Tries to withdraw to a different wallet, different PayPal, or different banking path

- Gets flagged, delayed, or asked for more proof

At that point, the trader thinks the broker is “suddenly difficult.”

In reality, they created a mismatch between funding and withdrawal expectations.

That doesn’t mean every delay is fair. It just means many delays are predictable.

This is also where account structure matters more than people realize. If you haven’t already, read which Capital Core account type fits your trading budget because the way you start often shapes how cleanly you manage deposits and withdrawals later.

Why Withdrawal Delays Happen Even When You Think You Did Everything Right

On paper, most traders assume the process is simple:

- submit withdrawal,

- wait a bit,

- receive funds.

In practice, “processed” and “received” are not the same thing.

Here’s how I interpret it as a trader:

- Requested = you submitted it

- Under review = internal checks may still be happening

- Processed = they approved and sent it

- Received = your wallet or payment provider actually delivered it

That distinction matters.

The most common real-world causes of delay

In my experience, these are the most realistic causes of delay on a broker like this:

- Your KYC was incomplete, old, blurry, or inconsistent

- Your address proof was rejected or expired

- Your phone wasn’t fully verified

- You used a different withdrawal method than the deposit route

- The name on the payment method didn’t match the account

- You used a high-friction payment method

- You requested a larger-than-usual first withdrawal

- Your account activity triggered manual review

- Your region requires additional compliance checks

- Your open trades or floating P/L complicated available balance review

Notice what’s not on that list:

- “The broker is automatically a scam because it took longer than expected”

I’m careful with that word.

A delay can be a red flag, yes. But a delay can also be a compliance bottleneck, a manual review, a payment rail issue, or a poor setup on the trader’s side.

That’s why I always judge the full sequence, not just the first 24–48 hours.

If you want a deeper companion read on that specific issue, I’d naturally point readers to my real Capital Core withdrawal timing test, because that’s where the emotional side of the payout wait becomes real.

My Personal Rule: First Withdrawal Is a System Test, Not a Profit Event

This is one of the most useful habits I’ve developed.

If I’m testing a broker like Capital Core, I do not treat the first withdrawal as “cashing out big.”

I treat it like this:

- small amount

- simple amount

- same method as deposit

- no open complications

- done early

That tells me more than a week of smooth trading.

If I deposit $50 or $100, I’d rather prove the process with a modest first withdrawal than build a larger balance and discover a preventable issue later.

That approach also fits the reality of low-entry brokers. Small-scale testing is practical, and honestly, it’s smarter than rushing in.

If you want to copy the same low-pressure approach I use, start small and make your first withdrawal a deliberate test instead of a high-emotion event: Open a Capital Core account and test it with a small amount first

And if you’re the kind of trader who gets tempted by promotions early, I’d also suggest reading whether the Capital Core 40% deposit bonus is worth it or risky before you click anything that changes your withdrawal conditions.

A More Honest Look at “Restrictions” on Capital Core

Most review articles say “restrictions may apply” and move on.

That’s too vague to be useful.

When I say restrictions in the context of the Capital Core verification process, I mean four very specific buckets.

1) Jurisdiction restrictions

Some countries naturally create more friction than others.

That doesn’t automatically mean you cannot use the platform.

But it does mean:

- more scrutiny,

- more requests for proof,

- slower reviews,

- and a higher chance your withdrawal becomes a compliance checkpoint.

If you are in a country with payment friction, sanctions exposure, e-wallet limitations, or frequent fraud flags, assume the burden of proof is higher.

2) Payment method restrictions

This is the big one.

Not every method behaves the same:

- PayPal has its own verification expectations

- Crypto has network and wallet handling issues

- Perfect Money is flexible but can still be scrutinized

- Some methods have different minimums and fees

That alone tells you the compliance bar is not identical across methods.

3) Name-match restrictions

If the account holder name on the funding route does not match the trading account, you’re asking for trouble.

This is where borrowed wallets, shared e-wallets, family accounts, or business/personal mismatches become painful.

4) Timing restrictions at withdrawal

Even if your account traded fine for days or weeks, the first meaningful withdrawal can trigger:

- extra document requests,

- payment ownership checks,

- manual phone verification,

- or account activity review

This is normal enough in the broker world that I build around it instead of pretending it won’t happen.

The Content Gap Nobody Explains Well: “Approved KYC” Doesn’t Always Mean “Fast Withdrawal”

This is one of the biggest blind spots I noticed when comparing broker help pages, review articles, and AI-generated summaries.

They often imply this simple formula:

KYC approved = withdrawals smooth

That’s incomplete.

A more realistic formula is:

KYC approved + payment method match + clean activity profile + consistent account details = better odds of smooth withdrawals

That’s a very different message.

And it’s much closer to how things actually work.

So if your KYC says “approved” but your withdrawal is delayed, the problem may not be your passport.

It may be:

- your wallet route,

- your source-of-funds logic,

- your country profile,

- your withdrawal size,

- or the fact that you’re trying to change the payout path after the fact.

That’s the kind of nuance most top-ranking pages skip.

If a reader is already skeptical at this stage, I’d naturally send them to my honest take on whether Capital Core is safe or a scam, because verification friction and broker trust are always connected in the trader’s mind.

What I’d Actually Do If a Capital Core Withdrawal Is Delayed

This is my real workflow when a withdrawal stalls.

I don’t panic on hour 12.

I don’t celebrate on hour 2 either.

I move in a sequence.

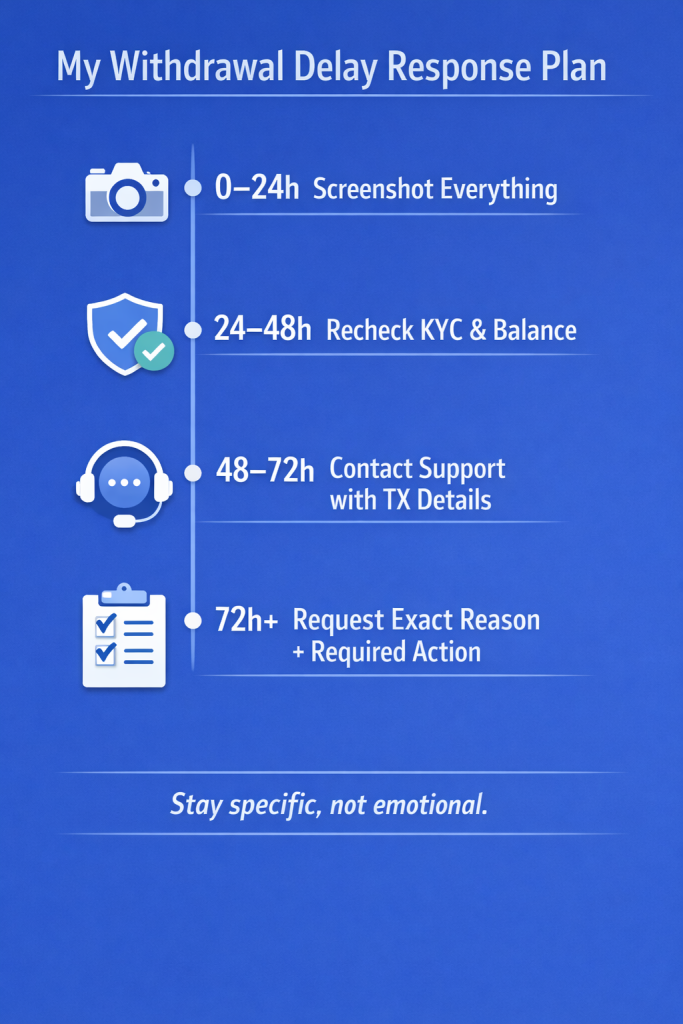

My delayed-withdrawal checklist

| Time since request | What I do | Why |

| 0–24 hours | Confirm request status, screenshot everything | Build a paper trail immediately |

| 24–48 hours | Recheck KYC status, verify no open issues | Make sure it’s not a simple account-side problem |

| 48–72 hours | Contact support with transaction details and deposit method used | Ask specific questions, not emotional ones |

| 72+ hours | Request explicit reason for delay and what document/action is needed | Force the case into concrete next steps |

| Ongoing | Save all emails, chat logs, IDs, TXIDs, timestamps | Essential if escalation is needed |

And here’s the wording I prefer:

- “Please confirm whether the withdrawal is pending due to KYC, payment method matching, or internal review.”

- “Please confirm whether any additional document is required.”

- “Please confirm whether my withdrawal method matches your AML requirement for original funding source.”

That wording matters.

It tells support you understand the framework, and it makes it harder for the conversation to stay vague.

How I’d Reduce the Odds of a Bad Surprise Before It Happens

If I were doing a careful Capital Core test this week, this would be my exact playbook.

My low-drama Capital Core setup

- Open the account in my real legal name only

- Verify phone first

- Upload ID and address proof before meaningful trading

- Pick one deposit method I can also use for withdrawal

- Avoid switching methods midstream

- Keep the first deposit modest

- Make a small first withdrawal early

- Save proof of every deposit and wallet transaction

- Avoid mixing accounts, names, or devices unnecessarily

- Scale only after the first withdrawal clears

That last point is the one I care about most.

I do not scale based on platform comfort.

I scale based on payout evidence.

If you’ve followed how I approach this broker, you already know I’m big on testing first and sizing later. The same logic shows up in my Capital Core $100 challenge notes, where the account size matters less than the process discipline.

And if you’re using outside trade help, I’d also connect this with what actually works with signals or bots on Capital Core, because inconsistent execution can create avoidable account behavior that complicates your review trail.

What I Think Traders Get Wrong About “Scam” vs “Friction”

I’ll be blunt here.

Some traders absolutely get treated unfairly in this industry. That happens.

But just as often, traders create preventable friction and then mislabel the entire event.

I’ve seen versions of this too many times:

- unverified phone

- different name on payment route

- deposit via one method, withdrawal via another

- no test withdrawal

- big first payout request

- then anger when it gets reviewed

That doesn’t automatically make the platform innocent. But it does make the situation more understandable.

That’s how I read it.

My Honest Take on the Capital Core Verification Process

If I had to summarize the Capital Core verification process in one sentence, it would be this:

It’s simple at the document level, but the real complexity shows up at the withdrawal level.

That’s the truth most ranking pages fail to explain.

The visible part is easy:

- upload ID

- upload proof of address

- verify phone

- maybe verify payment route

The invisible part is where traders get caught:

- same-name funding

- same-method withdrawal expectations

- region-based review intensity

- payment method limitations

- ongoing AML monitoring

- manual review when your behavior changes

So do I think the process is impossible? No.

Do I think it should be treated casually? Also no.

If you approach it like a grown-up operator instead of an impulsive trader, you reduce most of the avoidable problems.

If you’re still in the platform research phase, I’d also naturally weave in the binary setup I use on Capital Core, because strategy and withdrawal discipline need to work together, not separately.

My Practical Verdict: How I’d Use Capital Core Without Getting Overexposed

If I were advising a friend privately, I’d say this:

- Use a small deposit first

- Complete KYC before serious trading

- Choose the exit route before the entry route

- Don’t rely on “I can deposit, so I’m verified enough”

- Test the first withdrawal early

- Only increase size after a successful payout cycle

That’s the cleanest way to handle the Capital Core verification process without turning it into a trust fall.

And honestly, that’s how I now approach almost every broker that offers easy onboarding but has more layered withdrawal rules.

If you want to test Capital Core the way I would, keep it small, verify early, and let the first withdrawal decide whether the platform earns more of your capital: Open your Capital Core account here

Final Thoughts: The Trade Is Not Finished Until the Money Lands

I’ve become a lot less impressed by flashy broker features over time.

Tight spreads? Nice.

Bonuses? Fine.

Fast onboarding? Expected.

What I care about now is much simpler:

- Can I verify cleanly?

- Can I understand the restrictions before they matter?

- Can I withdraw without avoidable friction?

That’s why the Capital Core verification process deserves more attention than most traders give it.

The biggest mistake is assuming verification is a formality.

It isn’t.

On platforms like this, verification is part of the trading process itself. Not because it affects your chart, but because it affects whether your realized profit actually becomes spendable money.

And that’s the only finish line that counts.

If you decide to try Capital Core, do it like a tester, not a gambler. Open small, verify early, withdraw early, and only scale after the process proves itself in your own hands: Start with a small Capital Core account here